This is not a temporary adjustment. It is a fundamental realignment of what the industry’s biggest players choose to make. And while most market commentary focuses on the contraction, the closures, and the job losses, there is a parallel story that procurement leaders cannot afford to ignore. Every product line that is discontinued and every plant that is shuttered releases vast quantities of high-quality surplus intermediates into the market. For the right buyer, this is one of the most significant strategic sourcing opportunities in a generation.

Understanding the Pivot

To appreciate the surplus opportunity, it helps to understand the economics driving the pivot.

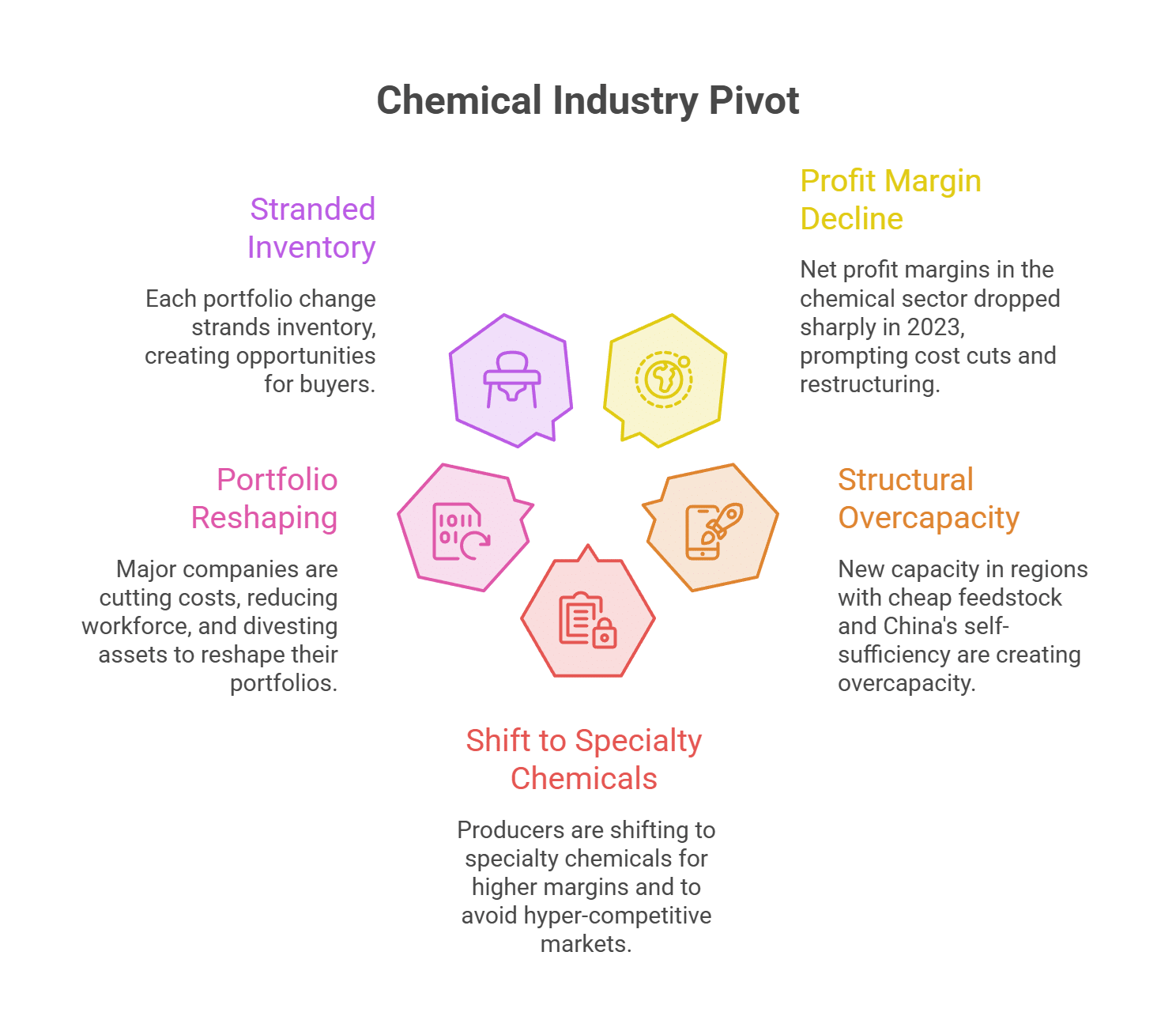

For two decades, net profit margins in the chemical sector averaged around 5.8%. Those margins dropped sharply beginning in 2023 and have remained under pressure, prompting producers to deploy aggressive cost cuts, restructurings, closures, and divestments [1]. The root cause is structural overcapacity in basic chemicals. New ethylene and polyethylene capacity continues to come online in regions with cheap feedstock, while China keeps building self-sufficiency in products like polypropylene [1]. For producers in higher-cost regions, competing in these commoditized markets has become a losing proposition.

The response has been a coordinated flight to specialty chemicals, which command higher margins precisely because they are less commoditized and avoid the hyper-competitive dynamics of the basic chemicals market [1]. Several major companies have publicly committed to shifting their portfolios away from basic petrochemicals and toward specialty or adjacent specialty products to capture better returns [1].

The scale of this restructuring is enormous. BASF has committed to cutting $2.7 billion in annual costs and reducing its workforce, and even sold its majority stake in its coatings business [2]. Dow announced thousands of additional job cuts as part of a $2 billion cost reduction effort. Solvay has closed multiple plants across Europe, and Celanese is targeting roughly $1 billion in total divestitures [2]. Each of these moves reshapes a portfolio, and each portfolio change strands inventory.

The Hidden Consequence: Orphaned Inventory

When a producer decides to exit a product line, the decision is made in a boardroom based on margin analysis and strategic focus. But the physical reality on the ground is messier. There are finished goods in the warehouse, work-in-progress materials in the pipeline, and intermediates that were destined for a now-discontinued process.

These materials do not simply disappear when a line is cut. They become orphaned inventory. The producer no longer has a use for them within its narrowed portfolio, and the original customers may have already been transitioned away or lost in the restructuring.

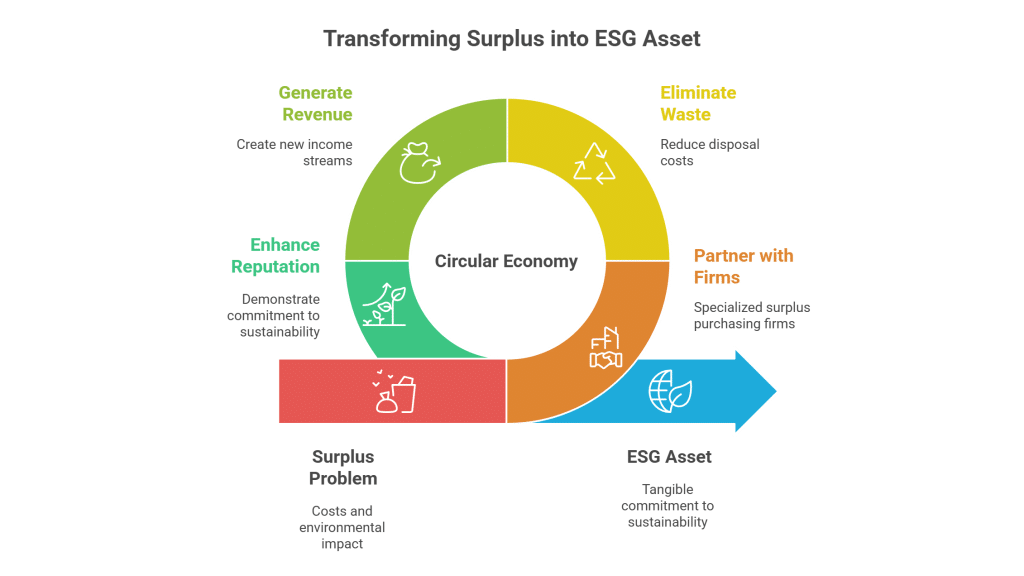

Historically, much of this orphaned material has been written off, discounted in fire sales, or sent for disposal. That is a profound waste. These are not low-grade leftovers; they are often high-quality specialty intermediates that simply no longer fit a producer’s strategic map. The embedded raw material investment, energy, and labor are all still locked inside them.

Why This Is a Goldmine for Buyers

For procurement teams and manufacturers, the specialty pivot creates a rare convergence of favorable conditions.

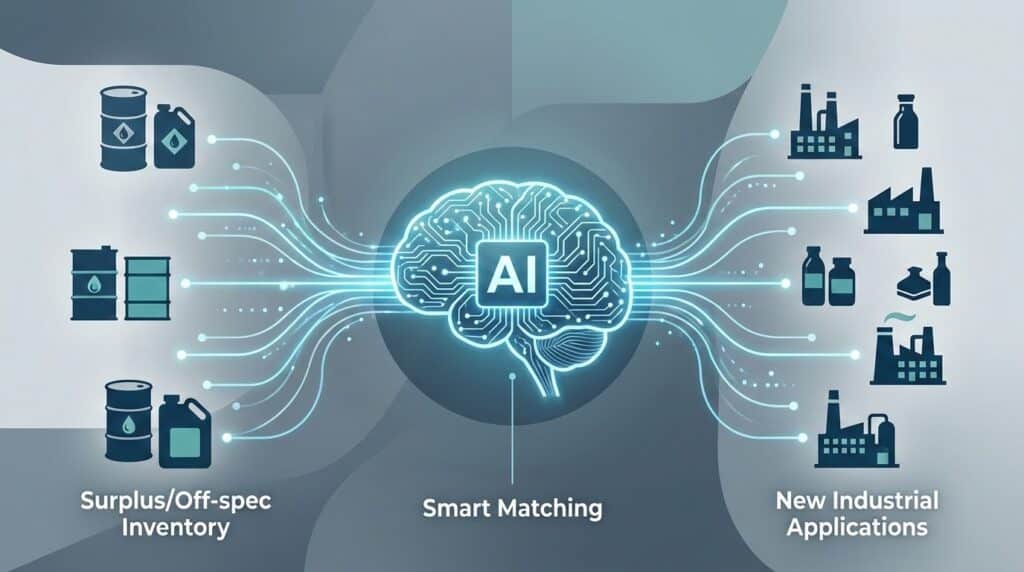

First, there is availability. Materials that were once locked inside a major producer’s catalog and only accessible through long-term supply agreements are suddenly on the open market. Specialty intermediates that might have been difficult to source through conventional channels become available as producers clear them out.

Second, there is price. Because this inventory is being released as a consequence of strategic exits rather than sold through virgin commodity channels, it is frequently available at a significant discount to standard market pricing. Buyers are effectively paying for the material, not the producer’s margin expectations.

Third, here is speed. Surplus intermediates are already manufactured and ready to ship. In an environment where plant closures are stretching lead times across the industry, the ability to source ready material without waiting on new production is a powerful advantage [3].

A Tale of Two Outcomes

Consider what happens to a specialty intermediate when a major producer decides its parent product line no longer fits the portfolio.

In the first scenario, the producer treats the inventory as a liability. It is written down, and a portion is sent for incineration or disposal. The raw material investment is destroyed, disposal fees are incurred, and a perfectly usable specialty chemical is removed from the economy entirely.

In the second scenario, the producer treats the inventory as a recoverable asset. Working through a surplus chemical network, the material is matched with a buyer who needs exactly those properties for an active production line. The producer recovers value, the buyer secures a scarce intermediate at an attractive price, and the embodied energy of the original production is preserved.

The difference between these two outcomes is not the material. It is the strategy and the network applied to it.

Turning Industry Contraction Into Procurement Advantage

The Great Specialty Pivot will continue throughout 2026 and likely accelerate as portfolio reevaluations drive a wave of consolidation beyond this year [1]. For forward-thinking buyers, this means the flow of surplus specialty intermediates is not a one-time event; it is becoming a structural feature of the market.

The companies that thrive in this environment will be those that stop viewing industry contraction purely as a risk and start treating it as a sourcing channel. Building relationships with surplus chemical partners who have the cross-industry knowledge to identify and qualify orphaned specialty intermediates is the key to unlocking this advantage.

At Surplus International, we specialize in capturing exactly this kind of inventory, the high-value intermediates and specialty stock released by a restructuring industry, and matching it with the manufacturers who need it most. The producers are reshaping their portfolios. The question for everyone else is whether they will see the surplus that pivot leaves behind as waste, or as opportunity.

References

[1] Deloitte Insights. (2025).2026 Chemical Industry Outlook Deloitte. Retrieved from https://www.deloitte.com/us/en/insןights/industry/chemicals-and-specialty-materials/chemical-industry-outlook.html

[2] Chemical & Engineering News. (2026). Chemical Industry Promises Another Year of Cutbacks. American Chemical Society. Retrieved from https://cen.acs.org/business/chemical-industry-promises-another-year-of-cutbacks/104/web/2026/02

[3] Alliance Chemical. (2026). Chemical Industry Faces Another Year of Deep Cutbacks as Major Producers Slash Thousands of Jobs. Retrieved from https://alliancechemical.com/blogs/news/chemical-industry-faces-another-year-of-deep-cutbacks-as-major-producers-slash