The global chemical industry is currently navigating one of its most significant periods of restructuring in recent history. Driven by a volatile macroeconomic environment, steep earnings declines, and persistent margin pressure, the world’s largest chemical producers are executing deep cost-cutting measures. While this consolidation presents challenges for traditional supply chains, it is simultaneously creating an unprecedented opportunity in the surplus chemical market.

The Scale of the Industry Pullback

The numbers defining this restructuring are staggering. According to recent industry analysis, major producers are aggressively shrinking their operational footprints to stabilize finances. BASF, the world’s largest chemical maker, reported a 38.8% drop in earnings in 2025 and has committed to cutting $2.7 billion in annual costs by the end of 2026, alongside eliminating 4,800 jobs [1].

Similarly, Dow Chemical has announced 4,500 job cuts as part of a $2 billion cost reduction effort following significant financial losses [1]. Other major players are following suit: Eastman Chemical is planning up to $150 million in additional cuts in 2026, Solvay has closed multiple plants across Europe, and Celanese is targeting $1 billion in total divestitures [1].

This is not a temporary dip; it is a fundamental realignment of global chemical manufacturing capacity.

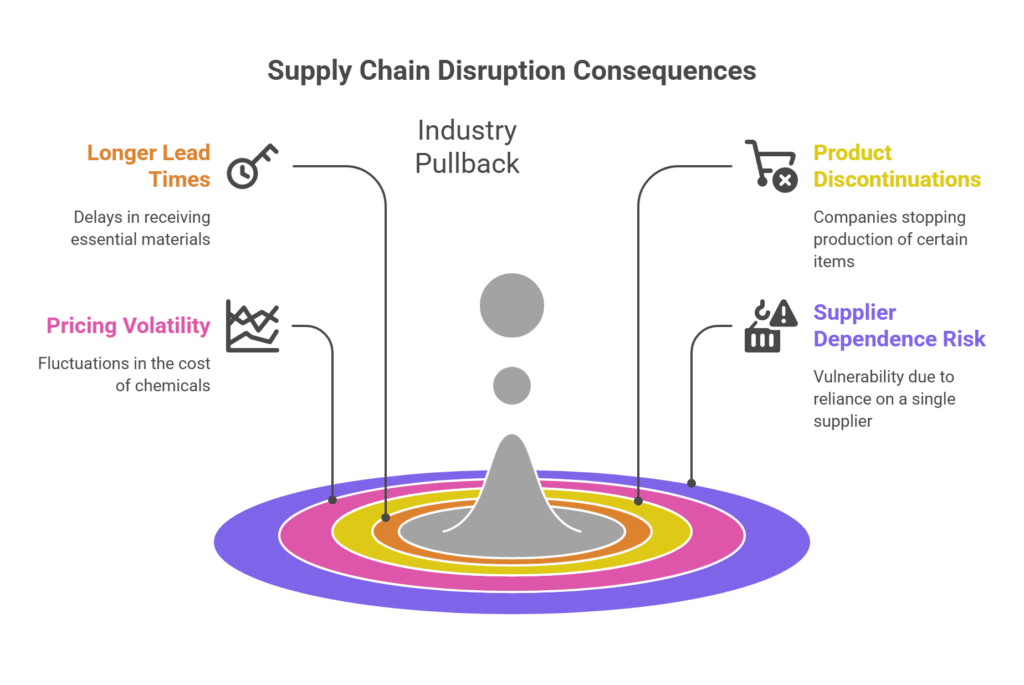

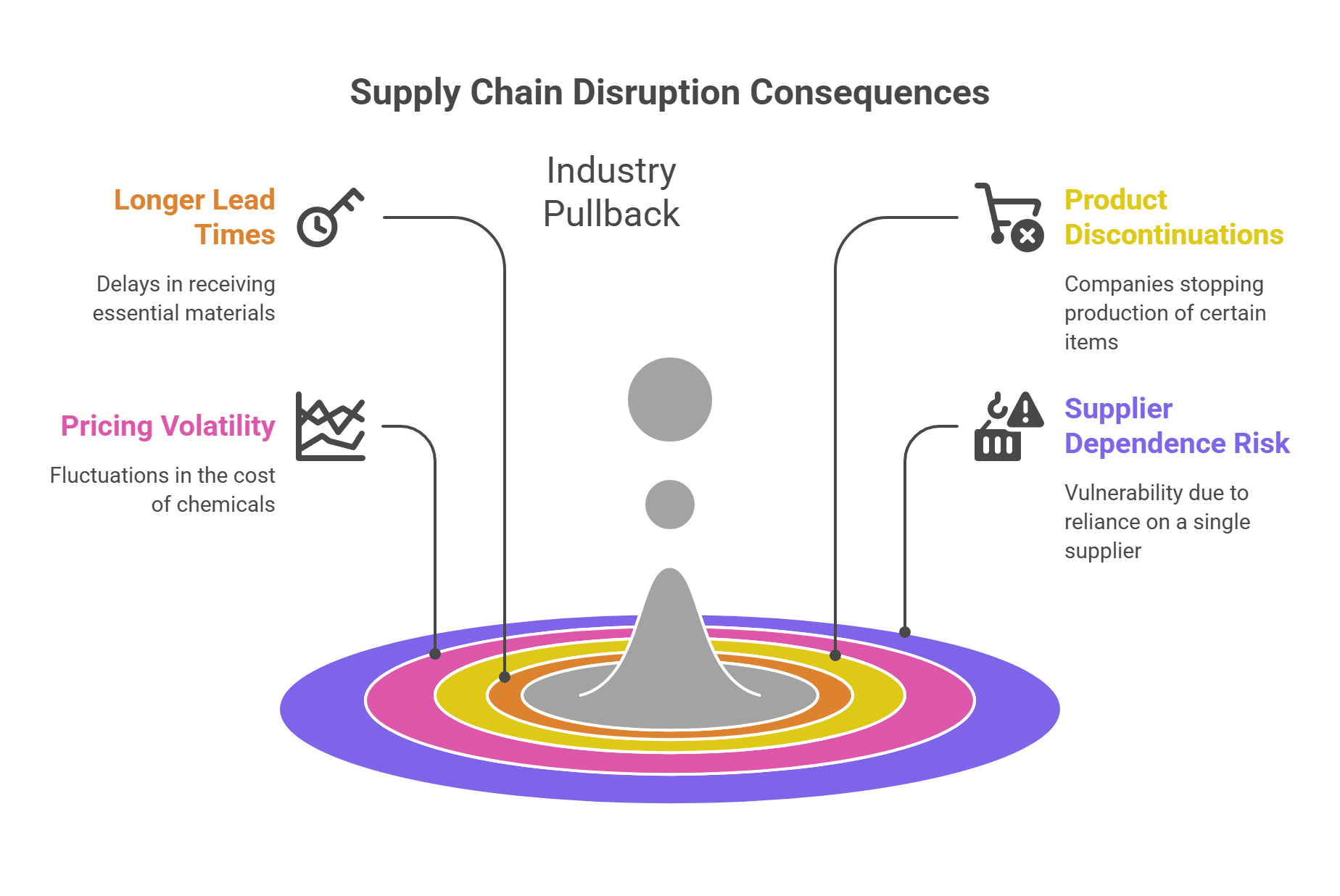

The Ripple Effect: Supply Chain Disruption

When industry titans close plants and exit non-core product lines, the effects ripple immediately through the supply chain. For procurement leaders and manufacturers reliant on these basic chemicals and polymers, this restructuring translates directly into operational risk.

Buyers are increasingly facing longer lead times as capacity comes offline. Product discontinuations are becoming more frequent as companies consolidate their portfolios to focus on high-margin sectors like healthcare and artificial intelligence [1]. Consequently, pricing volatility is spiking as reduced supply meets uneven demand.

For companies dependent on a single supplier for critical chemical inputs, this environment is highly precarious.

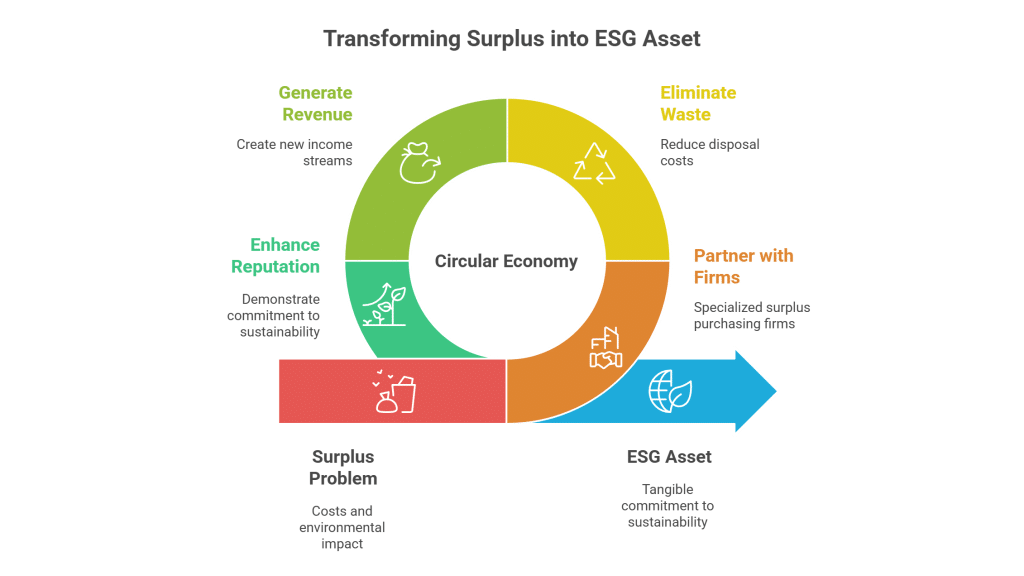

The Surplus Opportunity

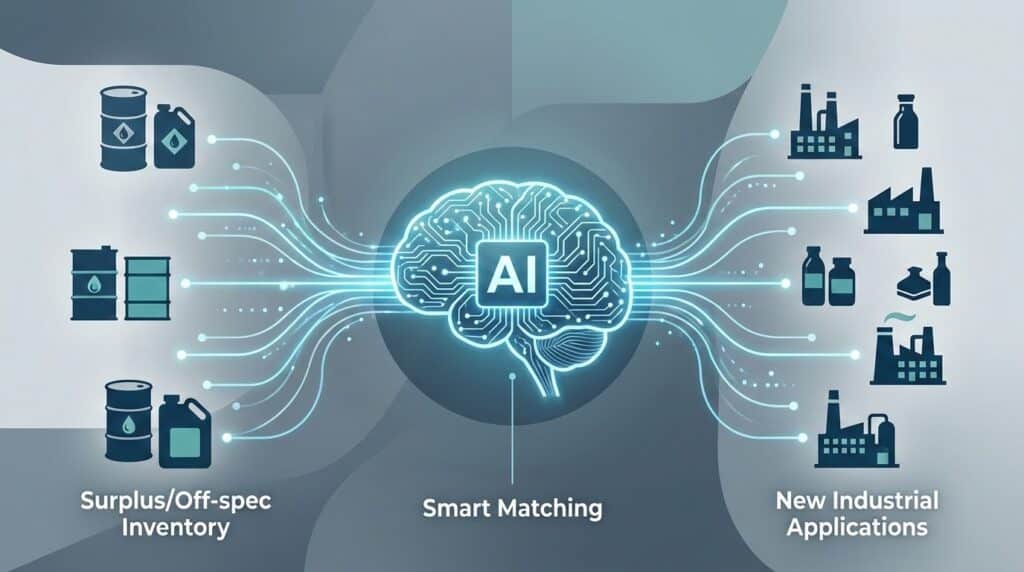

However, this disruption has a silver lining. When major facilities shut down or product lines are abruptly discontinued, massive volumes of chemical inventory do not simply disappear. They become surplus.

Currently, the market is being flooded with high-quality, off-spec, and excess chemical inventory resulting directly from these corporate restructuring efforts. For forward-thinking procurement teams, this represents a unique strategic advantage.

By tapping into the surplus market, companies can:

- Secure Supply: Bypass the extended lead times of traditional channels by sourcing materials that are already manufactured and ready to ship.

- Reduce Costs: Acquire essential chemicals at significant discounts compared to virgin market prices, protecting margins during a period of economic uncertainty.

- Enhance Resilience: Diversify sourcing strategies to mitigate the risk of single-supplier failures.

At Surplus International, we specialize in capturing this excess inventory and matching it with the manufacturers who need it most. We transform the industry’s restructuring friction into a reliable, cost-effective supply chain solution for our clients.

The chemical industry’s consolidation will likely continue throughout 2026. The companies that thrive will be those that adapt their procurement strategies to turn market disruption into a competitive advantage.

References

[1] C&EN (Chemical & Engineering News). (2026). Chemical Industry Promises Another Year of Cutbacks. American Chemical Society. Retrieved from https://cen.acs.org/articles/104/web/2026/02/chemical-industry-promises-another-year-of-cutbacks.html