Carbon Borders & Scope 3: How Surplus Chemical Sourcing Became a Compliance Strategy

For most of its history, the case for buying surplus and off-spec chemicals has been a financial one. Surplus material is cheaper than virgin product, it eliminates disposal costs, and it frees up warehouse space. These are real and durable advantages. But in 2026, a new and arguably more powerful argument has emerged, one that has little to do with the price tag and everything to do with regulation.

The convergence of carbon border taxes and intensifying Scope 3 emissions scrutiny has quietly transformed surplus chemical sourcing from a cost-saving tactic into a genuine compliance strategy. For procurement leaders managing both budgets and carbon disclosures, this changes the conversation entirely.

The New Regulatory Reality

Two regulatory forces are reshaping how global companies think about the carbon embedded in the materials they purchase.

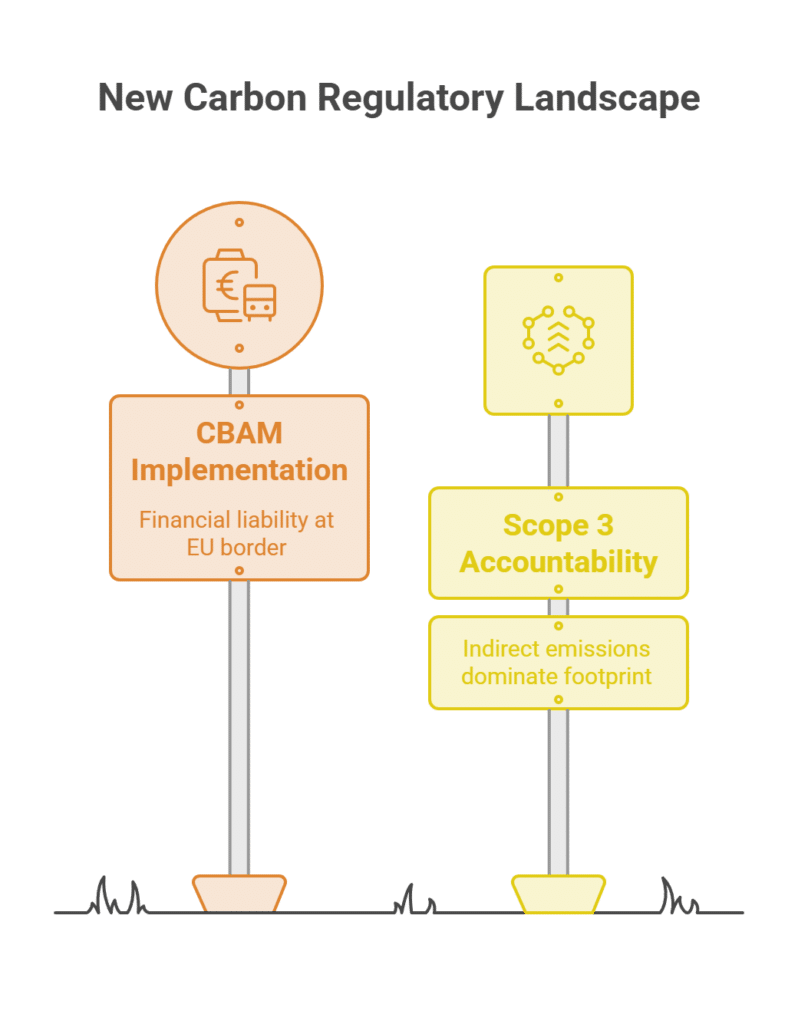

The first is the European Union’s Carbon Border Adjustment Mechanism, or CBAM. After a transitional reporting phase that ran from 2023 to 2025, CBAM entered its definitive regime on 1 January 2026 [1][2]. Under this definitive regime, financial liability becomes real: importers of covered goods must account for the greenhouse gas emissions embedded in their imports, with the first surrender of CBAM certificates scheduled for 2027 to cover emissions from goods imported during 2026 [3]. In practice, the carbon intensity of imported material now carries a direct financial cost at the EU border.

The second force is the steady tightening of Scope 3 emissions accountability. Scope 3 covers the indirect emissions that occur across a company’s value chain, outside its own operations [4]. For chemical companies in particular, upstream emissions from purchased goods and services represent a dominant share of the total footprint [5]. The scale is striking: research has found that for companies disclosing through major frameworks, Scope 3 emissions are on average many times larger than their direct operational emissions [6]. This is why purchased materials, rather than factory smokestacks, increasingly determine whether a company can meet its climate commitments.

Together, CBAM and Scope 3 reporting mean that the embedded carbon of a chemical input is no longer an abstract sustainability concept. It is a number that shows up in compliance filings and, increasingly, on the balance sheet.

The Embodied Carbon Advantage of Surplus

To understand why surplus chemicals fit so naturally into this new landscape, consider the concept of embodied carbon, the sum of all greenhouse gas emissions associated with extracting, processing, and manufacturing a material across its lifecycle [7].

Every kilogram of virgin chemical product carries a substantial embodied carbon burden. The chemical sector is one of the largest industrial energy consumers, with a significant share of that energy used as feedstock. Producing a new batch of a specialty chemical requires raw materials, process energy, and generates process emissions, all of which become part of that material’s embodied carbon.

Surplus and off-spec chemicals are fundamentally different in this respect. They already exist. The feedstock has been consumed, the energy has been spent, and the process emissions have already occurred, regardless of whether the material is used or destroyed. When a buyer sources a surplus or off-spec batch instead of commissioning new virgin production, they are effectively acquiring material whose manufacturing emissions have already been accounted for, rather than triggering a fresh cycle of emissions to make something new.

This creates a powerful and quantifiable advantage. Choosing surplus over virgin production avoids the embodied emissions of new manufacturing. For a buyer working to reduce the carbon intensity of its purchased goods, that is a direct, defensible improvement to its Scope 3 profile. And for a company managing CBAM exposure, sourcing lower-carbon-intensity material is precisely the kind of decision the mechanism is designed to reward.

A Lever That Moves Two Numbers at Once

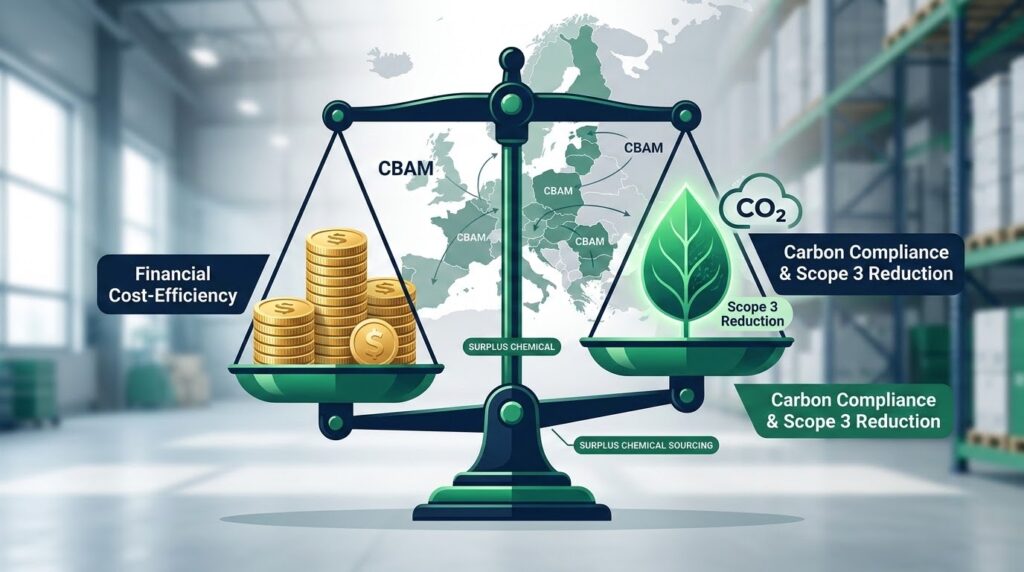

What makes surplus sourcing genuinely strategic in 2026 is that it is one of the rare levers that improves the cost line and the carbon line simultaneously.

Most decarbonization initiatives involve a trade-off. A company invests in cleaner energy, more efficient processes, or lower-carbon inputs, and accepts a higher cost in exchange for a lower footprint. Surplus sourcing inverts that logic. The buyer pays less for the material because it is priced on its surplus status, and at the same time reduces the embodied carbon associated with that purchase because no new production was triggered.

This dual benefit is why surplus is increasingly appearing not just in procurement strategies but in sustainability strategies. It allows a company to demonstrate progress against Scope 3 targets and manage CBAM-related costs without sacrificing margin, an alignment of financial and environmental incentives that is genuinely rare.

From Compliance Burden to Competitive Edge

The regulatory pressure is only intensifying. CBAM’s definitive regime is now live, Scope 3 disclosure expectations continue to broaden across jurisdictions, and major chemical producers are already working with their own suppliers to reduce upstream emissions [8]. Companies that treat these developments purely as a compliance burden will spend the coming years absorbing costs and scrambling to report.

The companies that recognize the opportunity will do something different. They will build surplus and off-spec sourcing into their procurement architecture deliberately, using it as a tool to manage carbon exposure as systematically as they manage cost. Doing so requires the ability to identify, qualify, and document suitable surplus materials, which in turn requires partners with deep cross-industry knowledge and the regulatory awareness to ensure compliance throughout.

At Surplus International, we help manufacturers capture exactly this advantage, matching high-quality surplus and off-spec inventory with the buyers who need it, and helping them turn the dual pressures of carbon borders and Scope 3 accountability into a measurable competitive edge. In 2026, the smartest procurement teams have stopped asking only what their chemicals cost. They are also asking what those chemicals cost the planet, and discovering that surplus sourcing answers both questions at once.

References

[1] European Commission, Taxation and Customs Union. Carbon Border Adjustment Mechanism. Retrieved from https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en

[2] KPMG. Navigating the EU Carbon Border Adjustment Mechanism (CBAM). Retrieved from https://kpmg.com/xx/en/our-insights/esg/carbon-border-adjustment-mechanism-cbam.html

[3] One Click LCA. CBAM: A Guide to the Carbon Border Adjustment Mechanism. Retrieved from https://oneclicklca.com/en-us/resources/articles/cbam-a-guide-to-carbon-border-adjustment-mechanism

[4] Brightest. (2026). The 15 Scope 3 Emissions Categories Explained. Retrieved from https://www.brightest.io/i/scope-3-categories-guide

[5] Nexio Projects. (2026). Mastering Scope 3 for the Chemical Sector: Upstream Emissions. Retrieved from https://nexioprojects.com/mastering-scope-3-for-chemical-sector-upstream-emissions/

[6] CO2 AI. (2026). CPG Scope 3 Emissions Suppliers: Why Your Carbon Data Determines Your Contracts. Retrieved from https://co2ai.com/insights/cpg-scope-3-emissions-suppliers-why-your-carbon-data-determines-your-contracts

[7] ACEEE. Embodied Carbon. Retrieved from https://www.aceee.org/embodied-carbon

[8] BASF. (2025). Partnering With Our Suppliers to Reduce Scope 3.1 Emissions. Retrieved from https://www.basf.com/global/en/who-we-are/organization/suppliers-and-partners/sustainability-in-procurement/product-carbon-footprint-of-raw-materials/Partnering-with-our-suppliers-to-reduce-Scope-3-1-emissions