India’s $87 Billion Chemical Import Bill: Why the World’s Fastest-Growing Market Needs Your Surplus Inventory

The International Energy Agency notes that the chemical sector is one of the largest industrial energy consumers, with a significant share of energy used as feedstock. When usable chemicals are discarded instead of reused, the embedded energy and value in those materials are lost.

India’s chemical industry is entering a new phase of growth, pressure, and opportunity.

On one side, the country is trying to strengthen domestic manufacturing, reduce import dependence, and build a more resilient chemical supply chain. On the other side, demand from downstream industries continues to rise faster than local supply can fully support.

That gap is visible in the numbers.

Recent industry reporting shows that India imported approximately $87.2 billion in chemicals, while exporting around $68.1 billion. This imbalance highlights a clear reality: India is not just a major chemical producer. It is also a major chemical buyer.

For North American manufacturers holding surplus, off-spec, slow-moving, or excess chemical inventory, this creates an important question:

Could materials sitting unused in one facility become critical supply for a buyer in India?

The answer is increasingly yes.

India’s Chemical Import Gap Is a Market Signal

A chemical import bill of more than $87 billion is not only a trade statistic. It is a signal of demand.

India’s economy depends on chemicals across thousands of downstream applications, including agriculture, pharmaceuticals, textiles, plastics, packaging, automotive components, construction materials, coatings, adhesives, and consumer goods. When chemical inputs become more expensive or difficult to source, the impact spreads far beyond the chemical industry itself.

This is why India’s chemical import dependency has become a strategic issue.

Government officials and industry leaders are pushing for greater self-reliance, but self-reliance does not happen overnight. Building local production capacity requires capital, infrastructure, technology, environmental compliance, skilled labor, and reliable access to raw materials.

In the meantime, Indian buyers still need feedstocks, intermediates, additives, solvents, resins, specialty chemicals, and other inputs to keep production moving.

That makes the global surplus market highly relevant.

India Wants to Build, But It Still Needs Supply

India has made clear that chemical and petrochemical manufacturing is a national priority.

The country’s “Make in India” strategy is designed to strengthen manufacturing infrastructure, encourage investment, and position India as a global manufacturing hub. In the chemical sector specifically, policymakers have discussed new support measures, including proposed chemical parks intended to strengthen domestic production capacity.

At the same time, India’s petrochemical demand is expected to grow significantly. Reuters reported that India expects major investment in its petrochemical sector over the coming decade, driven by rising demand from a growing middle class and expanding industrial base. India’s chemical and petrochemical sector has also been described as moving toward a value of around $300 billion.

This creates a dual reality.

India wants to produce more chemicals domestically. But until that capacity is built, qualified imports remain essential.

For Indian manufacturers, import substitution is a long-term goal. For day-to-day production, access to reliable chemical inputs is an immediate need.

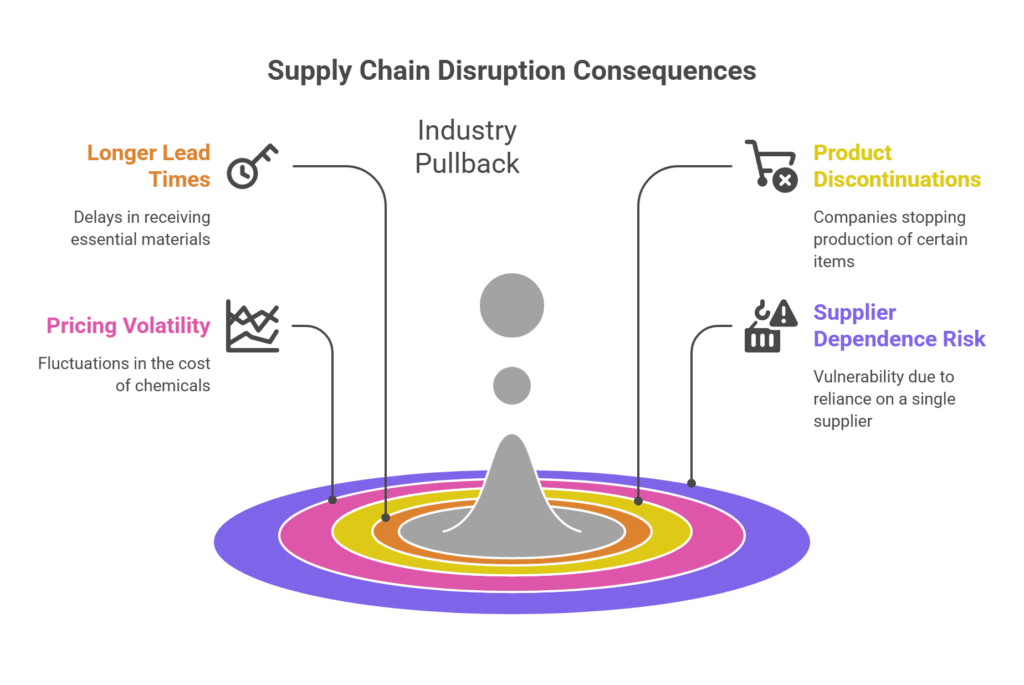

West Asia Volatility Has Made Chemical Sourcing More Urgent

The West Asia crisis has added another layer of urgency.

Supply chain disruptions, price volatility, freight uncertainty, and concerns around petrochemical feedstock availability have pushed Indian manufacturers and policymakers to rethink sourcing strategies. Industry bodies in India have reportedly asked the government to provide duty relief on key chemical feedstocks because of supply disruption concerns linked to the West Asia crisis.

This matters because many downstream manufacturers cannot simply wait for the market to stabilize. If a producer of coatings, adhesives, packaging materials, pharma intermediates, plastics, or textiles cannot access the chemicals it needs, production slows. Costs rise. Delivery timelines become less predictable.

In this environment, buyers become more open to alternative supply channels.

That is where surplus redistribution can play a strategic role.

A North American manufacturer may view excess inventory as a storage burden. An Indian buyer may view that same material as a valuable production input.

Anti-Dumping Reviews Show the Pressure on Indian Buyers

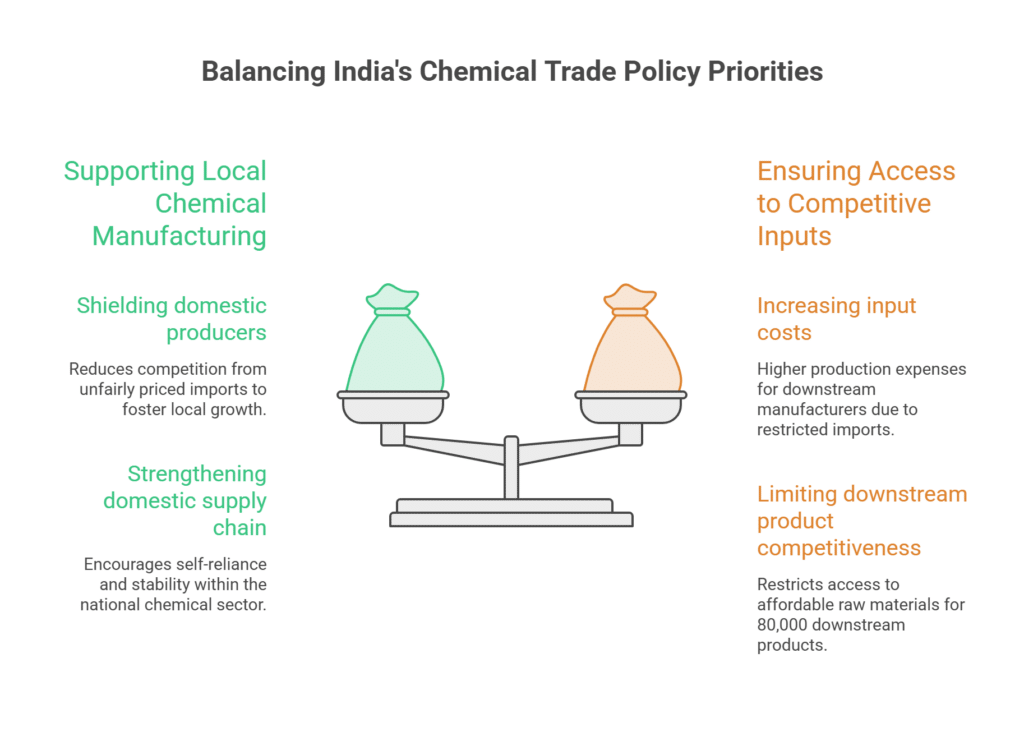

India’s chemical sector is also being affected by trade policy.

Anti-dumping duties are designed to protect domestic producers from unfairly priced imports. But when too many critical inputs become expensive or restricted, downstream manufacturers can face higher production costs.

Recent reporting shows that India’s anti-dumping framework is under scrutiny, especially in chemicals and allied industries. ET Chemicals reported that more than half of India’s active anti-dumping measures target chemicals or allied industries, with China being a major source of concern. Indian Express also reported that chemicals are used in nearly 80,000 downstream products in India, which means trade restrictions on chemical inputs can affect a very wide manufacturing base.

This does not mean India will stop protecting domestic producers. But it does show that policymakers are trying to balance two priorities:

- Supporting local chemical manufacturing.

- Ensuring downstream industries can access critical inputs at competitive prices.

For global suppliers, this creates a market that is actively searching for flexibility.

For surplus sellers, it creates an opening.

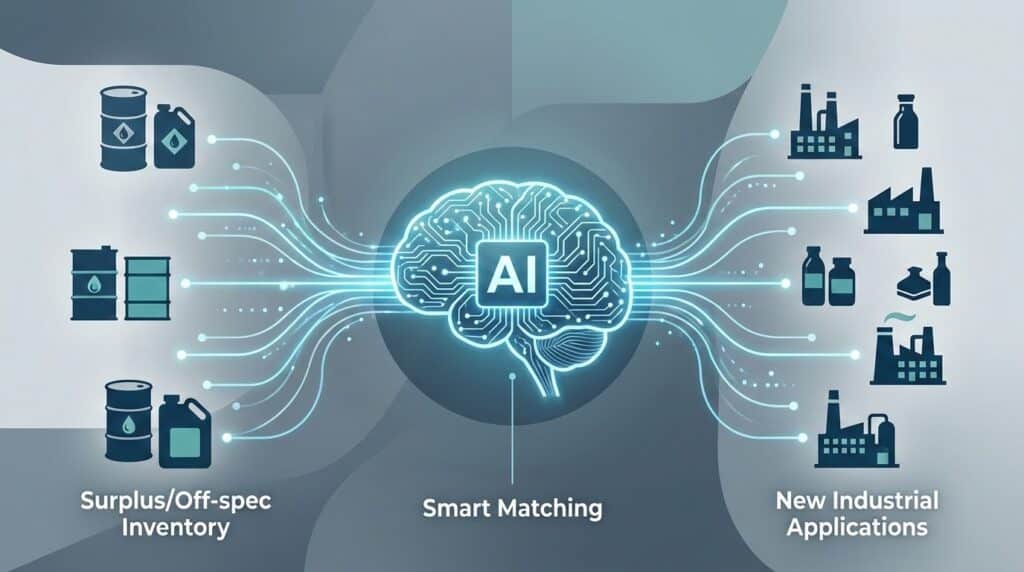

Why Surplus Inventory Fits This Moment

Surplus chemicals are often misunderstood.

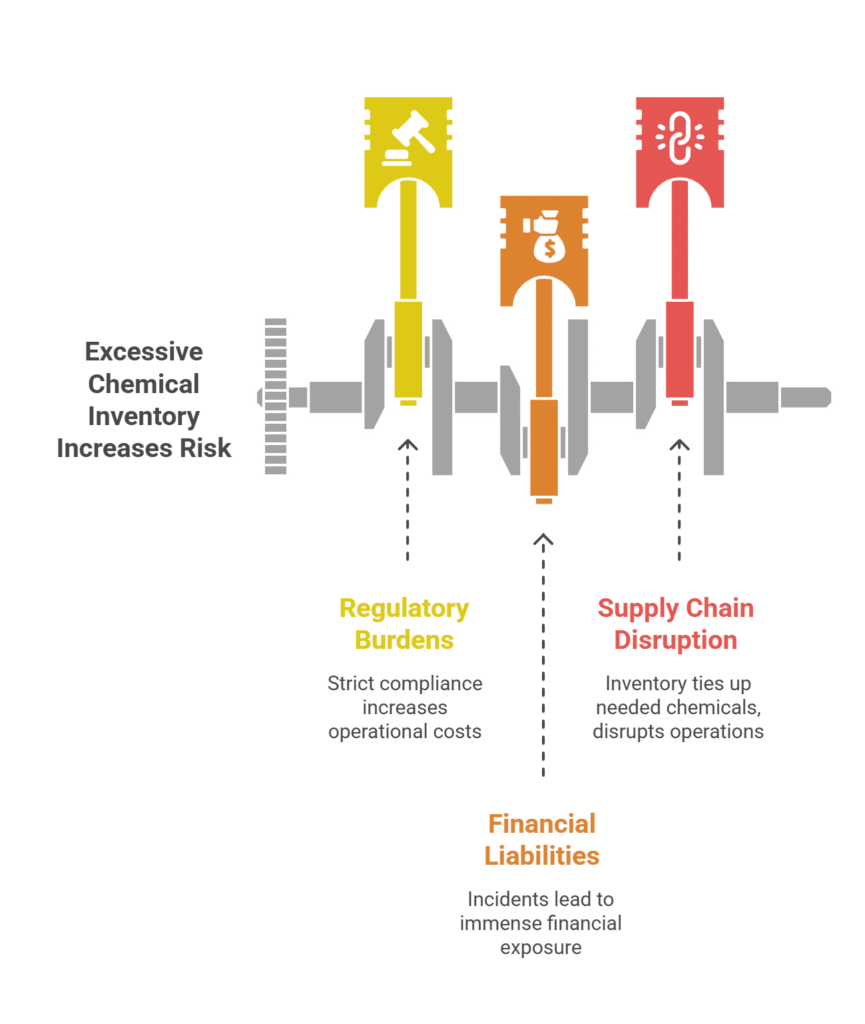

Many companies think of surplus inventory as a warehouse problem: materials that are not moving, taking up space, tying up capital, creating compliance obligations, and increasing storage risk.

But in the right market, surplus inventory is not waste.

It is supply.

Surplus materials may include:

- Excess inventory from overproduction

- Slow-moving raw materials

- Off-spec but usable chemicals

- Discontinued formulations

- Surplus intermediates

- Unused additives or specialty chemicals

- Materials from process changes or product line closures

- Packaged chemicals no longer needed by the original owner

In North America, these materials may sit in storage because they are no longer aligned with one company’s production plans.

In India, they may match an active need.

This is the logic behind surplus redistribution: moving usable chemical inventory from where it is idle to where it can create value.

The Benefits for North American Sellers

For North American manufacturers, surplus redistribution offers several advantages.

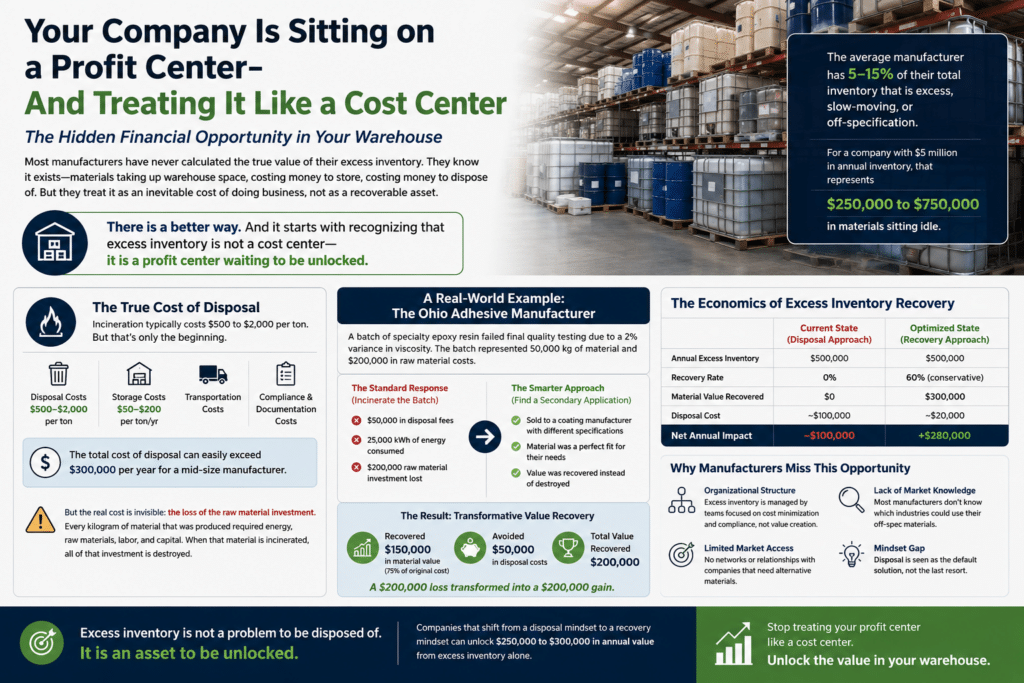

1. Recover Capital from Idle Inventory

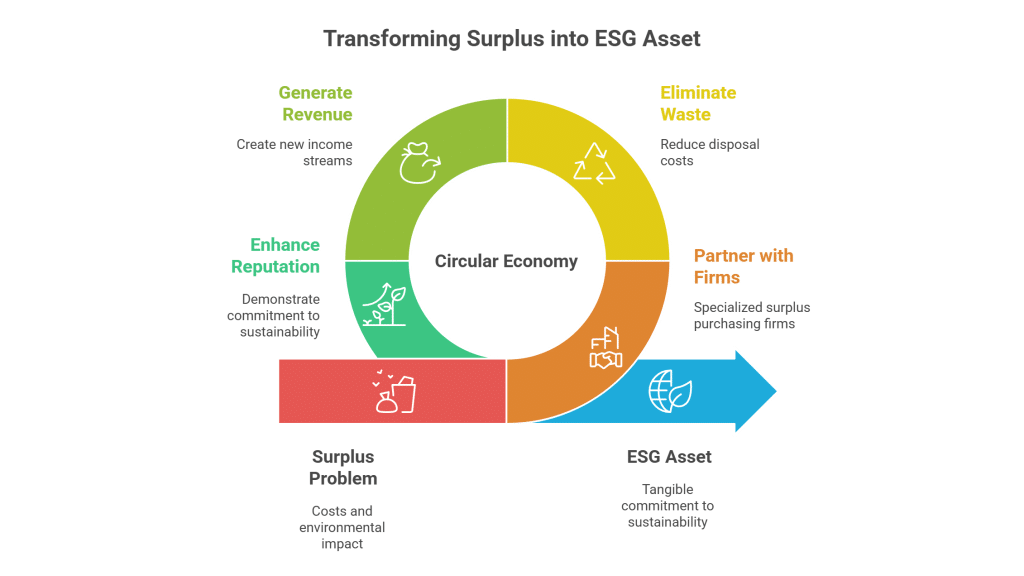

Unused inventory represents trapped value. Instead of writing off materials or paying for disposal, companies can recover part of their investment by selling usable chemicals into markets where demand exists.

2. Reduce Storage and Compliance Burden

Chemical storage is not passive. It requires monitoring, documentation, space, safety controls, environmental compliance, and often specialized handling. Reducing unnecessary inventory helps lower the operational burden on facilities.

3. Lower Risk Exposure

The longer hazardous or regulated chemicals remain in storage, the longer the company carries potential liability. Selling surplus materials can reduce the amount of chemical inventory on-site and help facilities manage risk more proactively.

4. Support Sustainability Goals

Redistribution supports circular economy principles by extending the useful life of already-manufactured chemicals. This can reduce the need for disposal and help avoid the environmental costs associated with producing replacement material from virgin feedstocks.

The International Energy Agency notes that the chemical sector is one of the largest industrial energy consumers, with a significant share of energy used as feedstock. When usable chemicals are discarded instead of reused, the embedded energy and value in those materials are lost.

The Benefits for Indian Buyers

For Indian chemical buyers, surplus inventory can provide a practical sourcing advantage.

1. Access to Needed Inputs

When supply chains are tight, surplus channels can provide access to materials that may be difficult, delayed, or expensive to source through traditional routes.

2. Cost Efficiency

Surplus materials can sometimes be acquired at attractive pricing compared with newly manufactured supply, depending on specification, volume, location, packaging, and urgency.

3. Supply Chain Flexibility

In a volatile global market, relying only on traditional sourcing channels can be risky. Surplus procurement gives buyers another option.

4. Faster Availability

If materials are already produced, packaged, and available for shipment, surplus sourcing may help reduce lead times compared with waiting for new production.

The Bridge Between Two Markets

The opportunity is clear, but it requires the right execution.

Selling surplus chemicals internationally is not simply a matter of finding a buyer. It requires product knowledge, documentation, regulatory awareness, logistics coordination, packaging review, and a trusted network of qualified buyers.

That is where Surplus International plays a critical role.

Surplus International helps connect companies holding excess, off-spec, or slow-moving chemical inventory with buyers that can use those materials. For sellers, this creates a path to recover capital and reduce inventory risk. For buyers, it creates access to chemical inputs that may support production in a volatile market.

In the context of India’s chemical import gap, this bridge becomes especially important.

North American manufacturers may be sitting on materials that no longer fit their own production needs. Indian manufacturers may be searching for those exact materials to support growth.

Surplus redistribution connects the two.

A Strategic Moment for Chemical Inventory Management

India’s $87 billion chemical import bill is not just an Indian issue. It is a global market signal.

It shows that one of the world’s fastest-growing manufacturing economies still needs reliable access to chemical inputs. It also shows that traditional sourcing strategies are under pressure from geopolitics, trade policy, and supply chain volatility.

For North American manufacturers, this is the time to reexamine surplus inventory.

Materials sitting in storage may have more value than expected. What looks like excess in one market may be needed supply in another.

In a world where chemical buyers are searching for resilience, surplus inventory is no longer just a recovery opportunity.

It is a strategic supply chain solution.

Frequently Asked Questions

India has a large and growing manufacturing base that depends on chemical inputs across many industries, including agriculture, textiles, pharmaceuticals, plastics, coatings, packaging, and automotive manufacturing. Domestic production is expanding, but demand remains high, creating continued reliance on imported chemicals.

Potentially relevant materials include feedstocks, intermediates, additives, solvents, resins, specialty chemicals, process chemicals, and other usable inventory that meets buyer specifications and regulatory requirements.

International buyers may have active demand for materials that are no longer needed domestically. Selling surplus inventory can help recover capital, reduce storage costs, lower compliance burden, and support sustainability goals by keeping usable materials in circulation.

Redistribution helps ensure that already-manufactured chemicals are used rather than discarded. This reduces waste and preserves the energy, raw materials, and production value already invested in those chemicals.

The first step is to catalog the inventory, confirm product specifications, review safety data sheets, check packaging and storage conditions, and work with a qualified surplus chemical partner that can evaluate market demand and connect the material with suitable buyers.

Sources

Source | What it supports |

ET Chemicals, May 2026 | India’s chemical imports of about $87.2B vs exports of $68.1B; import substitution and policy reform context. (ETChemicals.com) |

Economic Times, May 2026 | Chemicals Secretary Tejveer Singh urging self-reliance, concern over high imports, and proposed chemical parks. (The Economic Times) |

Reuters, Oct. 2024 | India’s expected petrochemical investment, sector growth, and production expansion outlook. (Reuters) |

ET Chemicals / WTO Trade Policy Review coverage, June 2026 | Anti-dumping measures and the share targeting chemicals/allied industries. (ETChemicals.com) |

Indian Express, May 2026 | West Asia crisis pressure, anti-dumping concerns, and chemical inputs affecting nearly 80,000 downstream products. (The Indian Express) |

Reuters, March 2026 | Example of India’s active anti-dumping investigations on chemical imports. (Reuters) |

IEA | Chemical sector as a major industrial energy consumer, supporting the embedded-energy/sustainability argument. (IEA) |

Make in India / PM India | India’s broader manufacturing infrastructure and investment strategy. (pmindia.gov.in) |