The PFAS Regulatory Wave How Surplus Markets Offer a Safe Harbor

The global chemical industry is currently managing one of the most complex regulatory transitions in its history: the phase-out and restriction of per- and polyfluoroalkyl substances (PFAS), commonly known as “forever chemicals.”

By mid-2026, the regulatory pressure has reached a critical inflection point. In June 2026, the European Chemicals Agency (ECHA) published the results of its draft consultation regarding the comprehensive PFAS restriction proposal, revealing deep industry concern-particularly from the electronics and semiconductor sectors, which accounted for the largest share of the 3,511 submitted comments [1]. Concurrently, the European Union’s Packaging and Packaging Waste Regulation (PPWR) is set to enforce strict PFAS limits on food-contact packaging starting August 12, 2026 [2].

In the United States, the regulatory environment is equally dynamic. While the EPA recently proposed extending compliance deadlines for certain PFAS drinking water standards, it continues to expand Toxics Release Inventory (TRI) reporting, which now covers over 200 PFAS compounds [3]. Furthermore, industry leaders are taking unilateral action; 3M completed its commitment to exit all PFAS manufacturing by the end of 2025, and BASF plans to follow suit by 2028 [4] [5].

This convergence of aggressive regulation and voluntary corporate exits is creating a massive supply chain shock. For procurement leaders and corporate restructuring teams, the PFAS transition is generating unprecedented volumes of orphaned inventory and triggering an urgent scramble for viable alternatives. In this turbulent environment, the surplus chemical market is emerging not just as a secondary option, but as a strategic safe harbor.

The Dual-Sided Supply Chain Shock

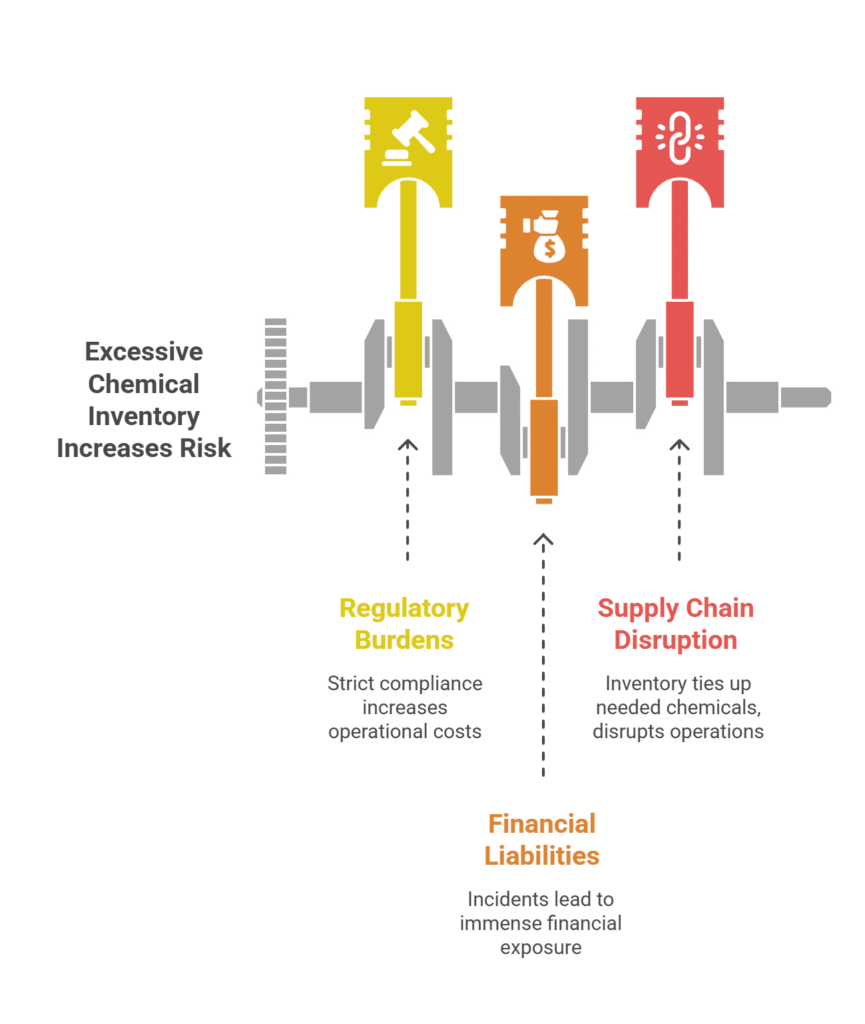

The PFAS phase-out creates two distinct, simultaneous challenges for the chemical supply chain: the liability of orphaned inventory and the urgent demand for alternatives.

- The Orphaned Inventory Liability

When a major manufacturer commits to phasing out PFAS, or when a new regional restriction takes effect, the supply chain does not instantly empty. Companies are frequently left holding substantial quantities of high-value PFAS inventory- ranging from specialized fluoropolymers to industrial coatings and aqueous film-forming foams (AFFF).

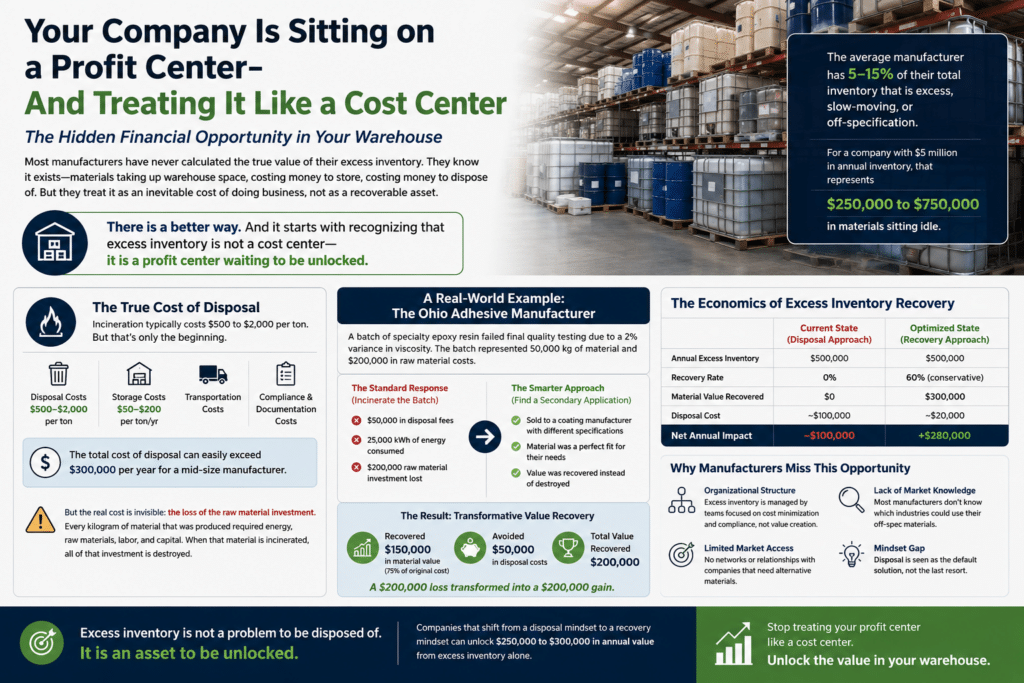

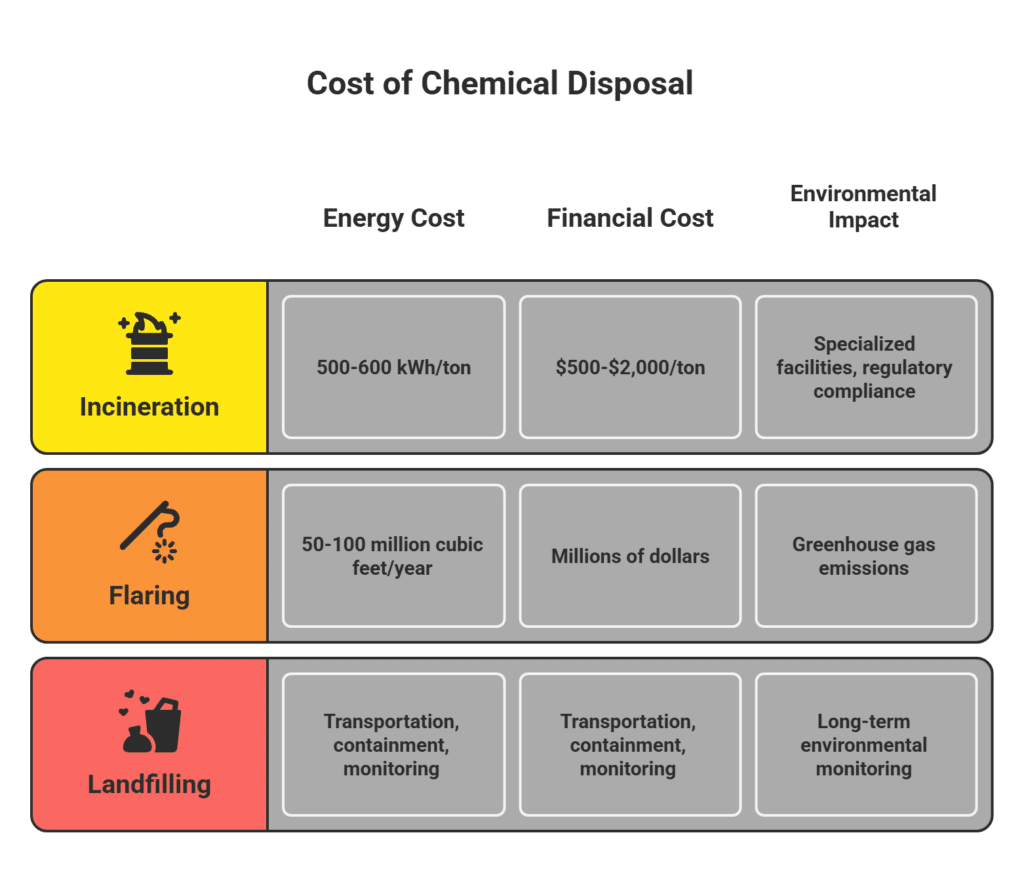

Historically, when a chemical faces regulatory restriction, the default corporate response is to write off the inventory and send it for specialized disposal. For PFAS, this is a financially devastating approach. Due to the very nature of these “forever chemicals,” their destruction requires extremely high-temperature incineration or advanced treatment technologies. Recent estimates indicate that the cost to treat PFAS-contaminated landfill leachate can range from 5 to 10 cents per gallon, and the broader corporate losses associated with PFAS contamination and remediation are projected to exceed $80 billion [6] [7].

Treating usable, high-value specialty chemicals as hazardous waste simply because they no longer fit a specific regional or corporate portfolio is a massive destruction of embodied value.

- The Urgent Demand for Alternatives

On the other side of the equation, manufacturers are racing to reformulate their products without PFAS. The global PFAS alternative chemicals market, valued at approximately $10.9 billion in 2025, is projected to grow to over $32 billion by 2035 [8].

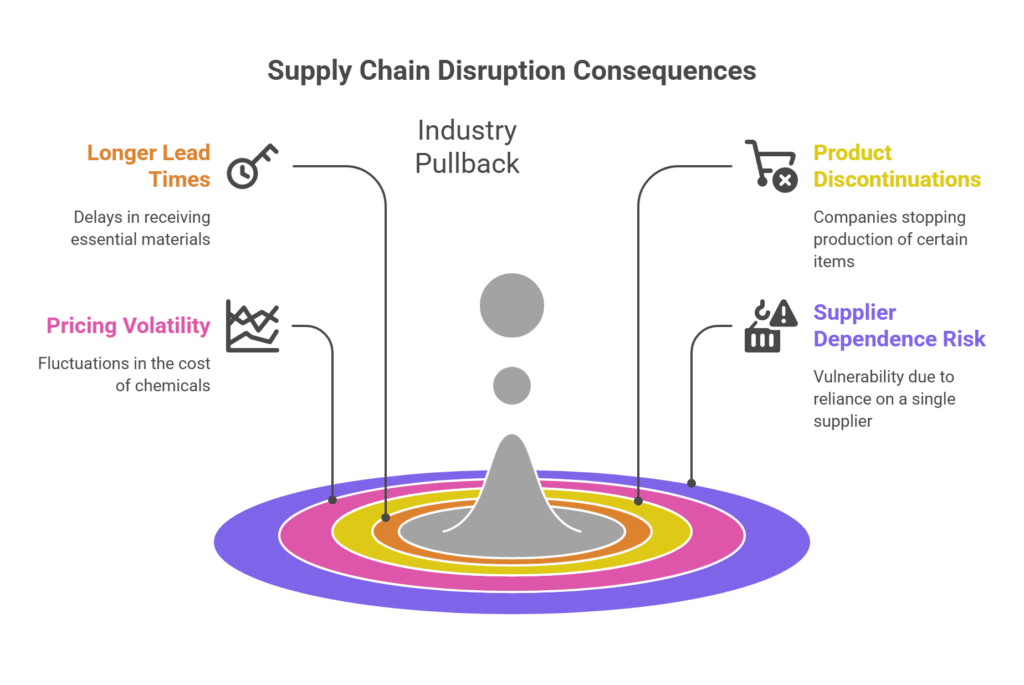

However, finding fully equivalent substitutes is notoriously difficult, particularly in cutting-edge fields such as semiconductor manufacturing (which relies on specific photoresists and etching gases), new energy batteries, and aerospace lubricants [1]. As companies transition to non-PFAS specialty chemicals, they are putting immense pressure on virgin supply chains, leading to extended lead times and price premiums for these highly sought-after alternatives.

How Surplus Networks Provide a Safe Harbor

Strategic surplus chemical sourcing provides a highly effective mechanism for managing both sides of the PFAS shock. By leveraging digital matchmaking and cross-border trade networks, companies can turn compliance liabilities into recovered capital and supply chain bottlenecks into sourcing opportunities.

Value Recovery Through Geographic Arbitrage

PFAS regulations are not uniform globally. While the EU is advancing a comprehensive ban and certain US states (like Maine and Minnesota) are enacting strict product-level restrictions, other jurisdictions have different timelines or exemptions. For example, some regions maintain exemptions for specific fluoropolymers like PTFE in critical industrial applications [9].

Surplus chemical networks allow companies holding orphaned PFAS inventory in a highly restricted region to legally and responsibly sell that material to buyers in regions or industries where its use remains permitted and essential. This geographic arbitrage transforms a disposal liability- which would cost the company money to destroy-into a revenue-generating asset recovery.

Sourcing Alternatives at the Speed of Surplus

For companies that urgently need compliant, non-PFAS specialty chemicals to meet impending regulatory deadlines (such as the August 2026 EU PPWR packaging rules), the surplus market offers a distinct advantage: speed.

As major producers restructure their portfolios and exit certain commodity or specialty lines, vast quantities of high-quality, non-PFAS intermediates enter the surplus market. Because this inventory is already manufactured and onshore, buyers can bypass the extended lead times of the virgin market. Procurement teams can secure the exact chemical profiles they need to reformulate their products quickly and often at a significant discount.

Use Case: Reformulating Food-Contact Packaging

In early 2026, a major European packaging manufacturer faced an impending crisis due to the EU PPWR mandate requiring PFAS-free food-contact packaging by August 12, 2026. Their primary supplier of a compliant, alternative barrier coating announced a six-month delay due to raw material shortages.

Facing a potential halt in production and loss of major retail contracts, the manufacturer utilized a digital surplus chemical exchange. The platform identified a matching batch of high-performance, PFAS-free synthetic wax (a known PFAS alternative) that had been orphaned following a strategic divestiture by a US-based specialty chemical firm. The manufacturer secured the surplus material within two weeks, ensuring full compliance with the PPWR deadline and avoiding millions in lost revenue. (Data based on EU PPWR compliance timelines and surplus market dynamics, 2026).

A Guide to Managing the PFAS Transition via Surplus Sourcing

To successfully navigate the regulatory wave and protect your balance sheet, procurement and compliance teams must proactively integrate surplus strategies.

The 5-Step Guide to PFAS Inventory Management:

- Conduct a Comprehensive Inventory Audit: Immediately identify all PFAS-containing materials within your supply chain, categorizing them by chemical structure, volume, and current regional regulatory status.

- Map the Regulatory Horizon: Cross-reference your inventory against impending deadlines, such as the EU PPWR restrictions or specific state-level bans, to determine the “shelf life” of your materials in their current markets.

- Engage a Surplus Network Early: Do not wait until a restriction takes effect to address orphaned inventory. Partner with a global surplus chemical network to identify legal, compliant secondary markets for your PFAS materials while they still hold value.

- Identify Alternative Profiles: Work with your R&D teams to define the precise chemical specifications required for your PFAS alternatives, ensuring you have a clear purchasing profile ready.

- Monitor the Surplus Market for Alternatives: Set up alerts within digital surplus exchanges for the specific non-PFAS specialty chemicals and intermediates you require, allowing you to secure compliant alternatives quickly and cost-effectively as they are released by industry restructuring.

Conclusion

The transition away from PFAS is inevitable, but the financial destruction associated with it does not have to be. As the regulatory wave intensifies through 2026 and beyond, the companies that thrive will be those that view the transition through a strategic, rather than purely reactive, lens.

By utilizing the surplus chemical market, organizations can avoid the exorbitant costs of specialized disposal, recover the embedded value of orphaned inventory, and rapidly source the compliant alternatives they need to stay competitive.

At Surplus International, we provide the network and the expertise required to turn the complexities of the PFAS phase-out into a strategic advantage. The regulations are changing, but with the right surplus strategy, your supply chain remains secure.

References

[1] CIRS Group. “ECHA Releases PFAS Restriction Draft Consultation Results: Electronics and Semiconductor Sector Draws Greatest Attention.” June 11, 2026. http://www.cirs-group.com/en/chemicals/echa-releases-pfas-restriction-draft-consultation-results-electronics-and-semiconductor-sector-draws-greatest-attention

[2] Anthesis Group. “PFAS In Packaging: EU PPWR Rules & Compliance.” 2025. https://www.anthesisgroup.com/insights/forever-chemicals-new-rules-pfas-compliance-under-the-eus-ppwr/

[3] JD Supra. “2026 mid-year PFAS update: How federal and state regulation is shaping compliance and litigation risk.” June 8, 2026. https://www.jdsupra.com/legalnews/2026-mid-year-pfas-update-how-federal-5089856/

[4] 3M. “3M to Exit PFAS Manufacturing by the End of 2025.” December 20, 2022. https://news.3m.com/2022-12-20-3M-to-Exit-PFAS-Manufacturing-by-the-End-of-2025

[5] ChemSec. “3M promised to phase out PFAS by the end of 2025. How has it turned out?” February 26, 2026. https://chemsec.org/3m-promised-to-phase-out-pfas-how-has-it-turned-out/

[6] Waste Dive. “Waste companies weigh costs – and benefits- of PFAS Superfund designation.” June 29, 2026. https://www.wastedive.com/news/pfas-contaminated-landfill-leachate-treatment-costs-technology-estimates/823977/

[7] Hinshaw & Culbertson LLP. “An Updated Primer on PFAS/Forever Chemical Claims.” November 14, 2024. https://www.hinshawlaw.com/en/insights/insights-for-insurers-alert/commentary-an-updated-primer-on-pfasforever-chemical-claims-regulation-litigation-large-losses-and-insurance-coverage-issues

[8] MarketResearch.com. “PFAS Alternative Chemicals Market Opportunity, Growth.” December 2025. https://www.marketresearch.com/One-Off-Global-Market-Insights-v4130/PFAS-Alternative-Chemicals-Opportunity-Growth-44982475/

[9] PackagingLaw.com. “New Mexico Joins Maine and Minnesota in Enacting Bans on PFAS.” April 24, 2025. https://www.packaginglaw.com/news/new-mexico-joins-maine-and-minnesota-enacting-bans-pfas-food-packaging-and-cookware