The narrative surrounding this shift is overwhelmingly positive: reshoring promises greater control, reduced geopolitical risk, and a revitalization of domestic industrial bases. However, for procurement leaders in the chemical sector, this geographic pivot exposes a critical execution gap. Simply moving a factory to North America does not automatically confer supply chain resilience. If that facility remains tethered to rigid, virgin-only procurement models while global shipping lanes remain volatile, the supply chain is not fixed- the bottleneck has merely been relocated.

To truly secure the benefits of reshoring, manufacturers must integrate an agile layer into their procurement strategies. Increasingly, that agile layer is being built on the strategic sourcing of surplus chemicals.

The Vulnerability of the Reshored Supply Chain

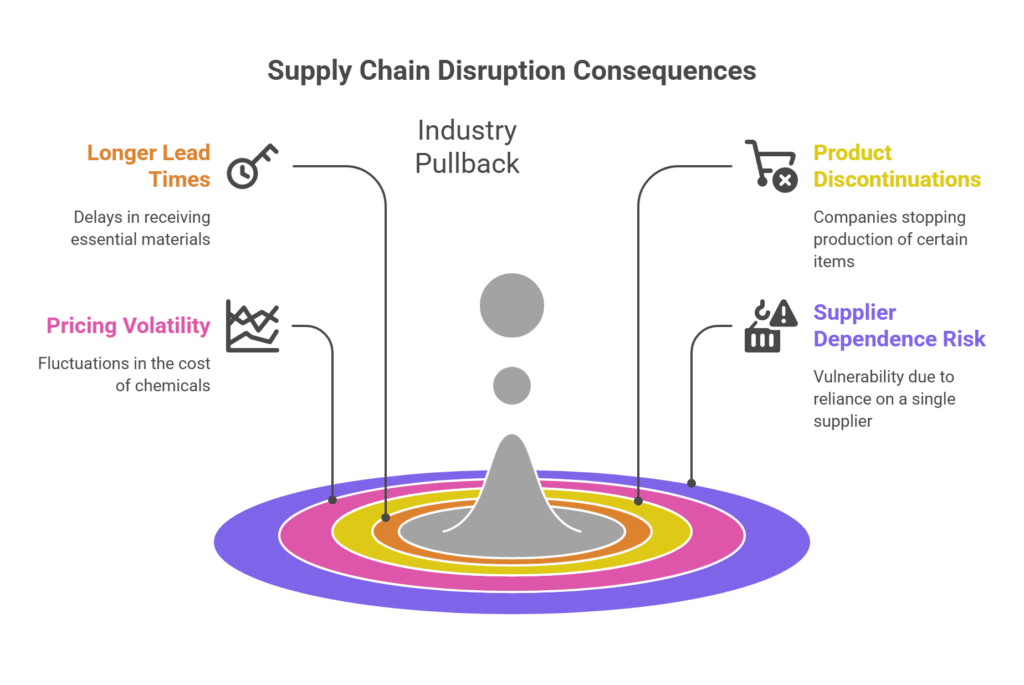

The core challenge for newly reshored or nearshored facilities is that while the final assembly or formulation may happen domestically, the upstream supply chain often remains highly globalized and vulnerable.

In mid-2026, the physical realities of global trade are stark. Tensions around the Strait of Hormuz and the Red Sea have forced major carriers to reroute vessels around the Cape of Good Hope, adding one to three weeks of transit time and significant conflict-related surcharges to shipments [2]. Simultaneously, the trans-Pacific shipping market is facing extreme capacity shortages as retailers frontload goods [3].

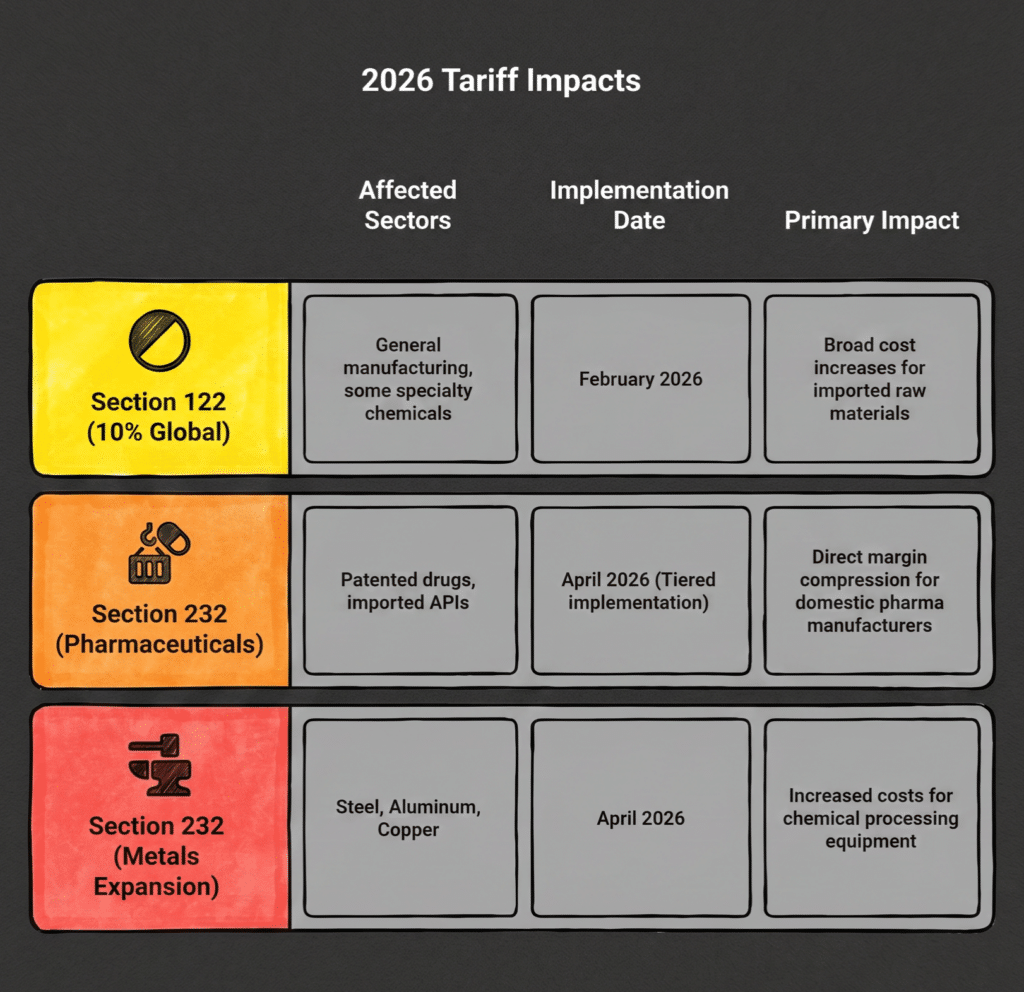

Furthermore, trade policy remains highly reactive. With the definitive regime of the EU’s Carbon Border Adjustment Mechanism (CBAM) now live and ongoing tariff volatility- including the recent Supreme Court tariff rulings under review by the American Chemistry Council – the cost predictability of imported raw materials has deteriorated [4] [5].

For a domestic manufacturer, relying exclusively on imported virgin feedstocks in this environment means accepting unpredictable lead times and volatile costs. A reshored plant cannot operate efficiently if its raw materials are stuck on a rerouted vessel or subjected to sudden tariff spikes.

The Restructuring Catalyst: A Surge in Domestic Surplus

Simultaneously, the chemical industry is experiencing a massive structural realignment that is creating a unique opportunity for domestic buyers.

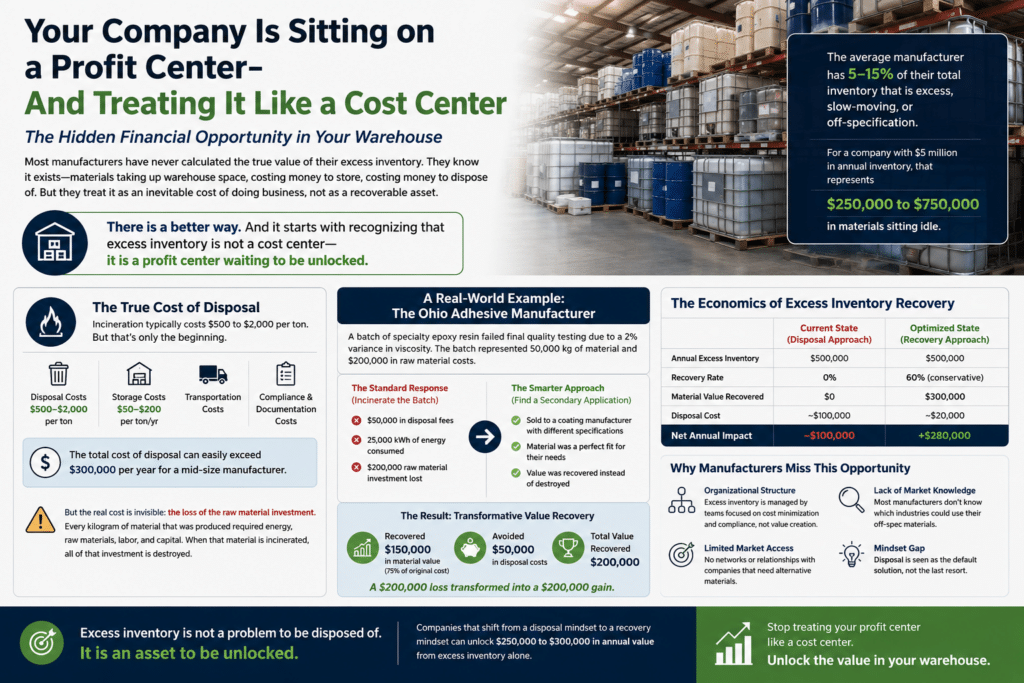

Faced with persistent overcapacity in basic chemicals and compressed margins, major producers are aggressively restructuring their portfolios. A recent analysis highlights that more than 120 publicly announced chemical plant closures have occurred since 2022, fundamentally altering the production landscape [6]. Major players like BASF, Dow, and Solvay have executed significant cost-reduction programs and plant shutdowns [7].

While these closures represent a contraction in overall capacity, they also trigger the release of unprecedented volumes of orphaned inventory. When a product line is discontinued or a plant is decommissioned, the high-quality specialty intermediates, off-spec materials, and raw materials left behind enter the surplus market.

This restructuring-driven surplus is a goldmine for reshored manufacturers. It represents high-quality, domestic inventory that is already manufactured, already onshore, and ready to deploy.

Why Surplus is the Agile Layer of Reshoring

Integrating surplus chemical sourcing into a procurement strategy provides the flexibility that rigid supply chains lack. This approach functions as a critical buffer for three primary reasons:

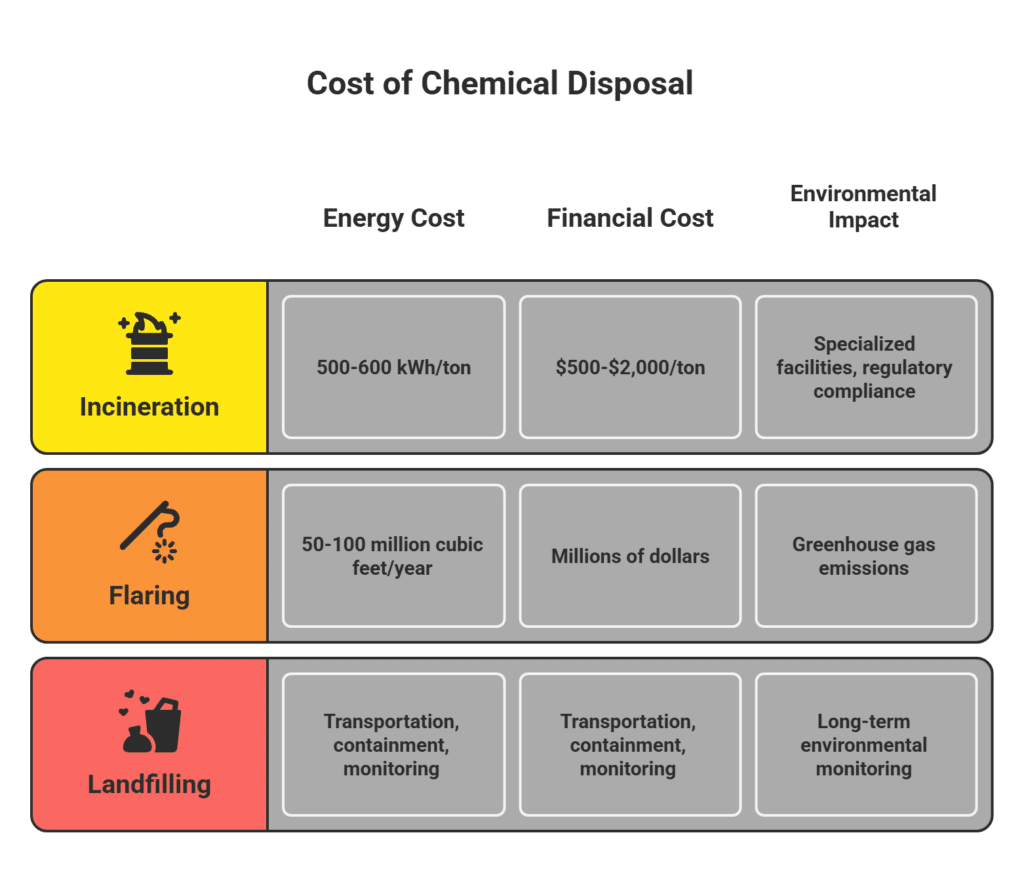

- Decoupling from Freight Volatility: Domestic surplus inventory sidesteps the Hormuz and Red Sea reroutes, capacity shortages, and extended transit times affecting imported chemicals. When ocean freight becomes unpredictable, ready domestic material ensures production lines keep running.

- Insulation from Tariff Swings: Surplus and off-spec chemicals are typically priced based on their surplus status rather than virgin commodity indices. This shields buyers from sudden tariff-driven cost increases that impact imported virgin feedstocks, offering a degree of price predictability essential for accurate forecasting.

- Speed to Market: Because surplus inventory is already manufactured, it directly counters the longer lead times created by industry-wide plant closures and shipping delays. When a manufacturer needs material immediately to cover a supply gap, domestic surplus is often the fastest viable option.

“In 2026, disruptions are no longer isolated events. Geopolitical conflicts, climate volatility, cyber risks, and growing supply chain complexity are reshaping how companies operate.” [8]

In this environment, rigidity is a liability. Surplus sourcing provides the necessary elasticity.

Real-Time Market Application: The Automotive Sector

Use Case: Mitigating Supply Shocks in Automotive Coatings

In early 2026, a major North American automotive manufacturer faced critical shortages of specific specialty resins used in their advanced coating formulations due to trans-Pacific shipping delays. Traditional virgin suppliers quoted lead times exceeding eight weeks.

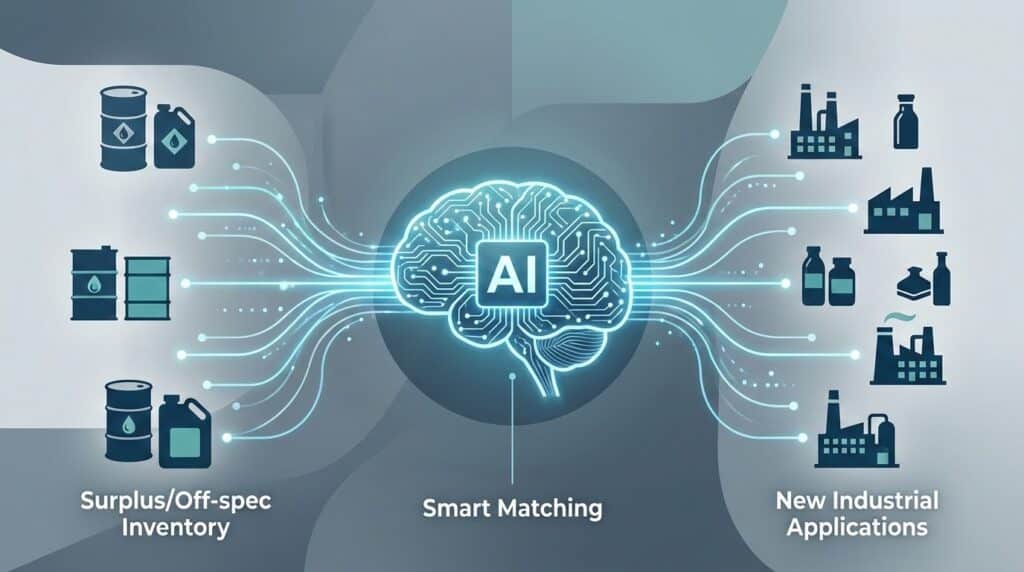

By utilizing a digital surplus chemical marketplace, the manufacturer’s procurement team identified a matching batch of high-quality, off-spec resin released during a recent plant decommissioning by a major European chemical producer’s US subsidiary. The surplus material was secured and delivered within days at a 30% discount to virgin market prices, preventing a costly production halt. This highlights how digital matching technologies are instrumental in transforming orphaned inventory into immediate supply chain solutions. (Data referenced from general industry supply chain resilience models, 2026).

A Guide to Integrating Surplus into Procurement

To leverage surplus chemicals as a strategic hedge in a reshored supply chain, procurement leaders must move beyond ad-hoc purchasing and build systematic processes.

The 5-Step Guide to Strategic Surplus Sourcing:

- Identify Critical Vulnerabilities: Map your bill of materials to identify which essential inputs are most exposed to global shipping delays, tariff volatility, or single-source dependency.

- Define Acceptable Variances: Work with your technical and formulation teams to determine the exact specifications required and where off-spec or alternative grades could be successfully utilized without compromising the final product.

- Establish Network Partnerships: Build relationships with established surplus chemical networks and digital marketplaces that have visibility into domestic inventory released by plant closures and restructuring.

- Implement Rapid Qualification: Develop an expedited quality assurance protocol to quickly test and qualify surplus batches when they become available, ensuring you can act fast before the inventory is claimed.

- Track Carbon and Cost Benefits: Document the financial savings and the Scope 3 emissions reductions achieved by sourcing surplus (which avoids the embodied carbon of new production), integrating these metrics into your corporate sustainability reporting.

Conclusion

The push to reshore manufacturing is a necessary step toward greater industrial resilience, but geography alone cannot solve the complexities of the 2026 chemical market. As global supply chains face persistent disruption and the chemical industry undergoes historic restructuring, procurement strategies must adapt.

Surplus chemical sourcing is no longer just a tactic for cost reduction; it is a strategic imperative for supply chain continuity. By treating domestic surplus inventory as a core component of their procurement architecture, manufacturers can build the agile layer required to make reshoring a reality.

At Surplus International, we specialize in capturing this high-value orphaned inventory and matching it with the manufacturers who need it most. In the new era of domestic manufacturing, the smartest supply chains are the ones that know how to utilize what is already here.

References

[1] UK Government. “Annex A – Evidence and trends for supply chain vulnerability and resilience.” Global supply chains: a foresight report on risk and resilience. June 15, 2026. https://www.gov.uk/government/publications/global-supply-chains-a-foresight-report-on-risk-and-resilience/annex-a-evidence-and-trends-for-supply-chain-vulnerability-and-resilience

[2] S&P Global Ratings. “European Chemicals: Hormuz Reopening Could Offset Fading Middle East Tailwinds.” June 10, 2026. https://www.spglobal.com/ratings/en/regulatory/article/european-chemicals-hormuz-reopening-could-offset-fading-middle-east-tailwinds-s101687428

[3] Facebook. “Trans-Pacific shipping market faces extreme capacity shortages in 2026.” June 17, 2026. https://www.facebook.com/groups/1115522112568801/posts/2227788811342120/

[4] Surplus International. “Carbon Borders & Scope 3: How Surplus Chemical Sourcing Became a Compliance Strategy.” 2026. https://surplus-inter.com/carbon-borders-scope-3-how-surplus-chemical-sourcing-became-a-compliance-strategy/

[5] American Chemistry Council. “ACC Statement on Supreme Court Tariff Ruling.” June 30, 2026. https://www.americanchemistry.com/chemistry-in-america-industry-innovation-impact/news-trends/press-release/2026/acc-statement-on-supreme-court-tariff-ruling

[6] WSI. “WSI’s Warehouse Wire: June 26, 2026.” June 26, 2026. https://www.wsinc.com/blog/wsi-warehouse-wire-june-26-2026/

[7] Surplus International. “The Great Specialty Pivot: Why Producers Abandoning Commodity Lines Is a Goldmine of Surplus Intermediates.” 2026. https://surplus-inter.com/the-great-specialty-pivot-why-producers-abandoning-commodity-lines-is-a-goldmine-of-surplus-intermediates/

[8] LinkedIn. “Supply Chain Disruptions 2026: Building Logistics Infrastructure.” June 11, 2026. https://www.linkedin.com/pulse/supply-chain-disruptions-2026-building-logistics-si8af