The Two-Speed Market: Overcapacity Meets Recovery, and Why Surplus Is the Smartest Hedge in 2026

The 2026 chemical market is defined by contradictory signals, creating a “two-speed” landscape for procurement teams.

Structural overcapacity suppresses some segments, while manufacturing growth drives a tentative recovery in others. Layered on this complexity are unpredictable tariffs and severe shipping disruptions that make rigid supply chains a significant liability. In this environment, relying solely on long-term virgin contracts exposes your organization to unnecessary risk.

Instead, smart procurement leaders are pivoting toward flexibility to maintain reliable supply lines. Surplus and off-spec inventory has emerged as a critical hedge, offering stability where standard chains cannot.

Discover why it is time to rethink your sourcing strategy to stay competitive and supplied throughout the year!

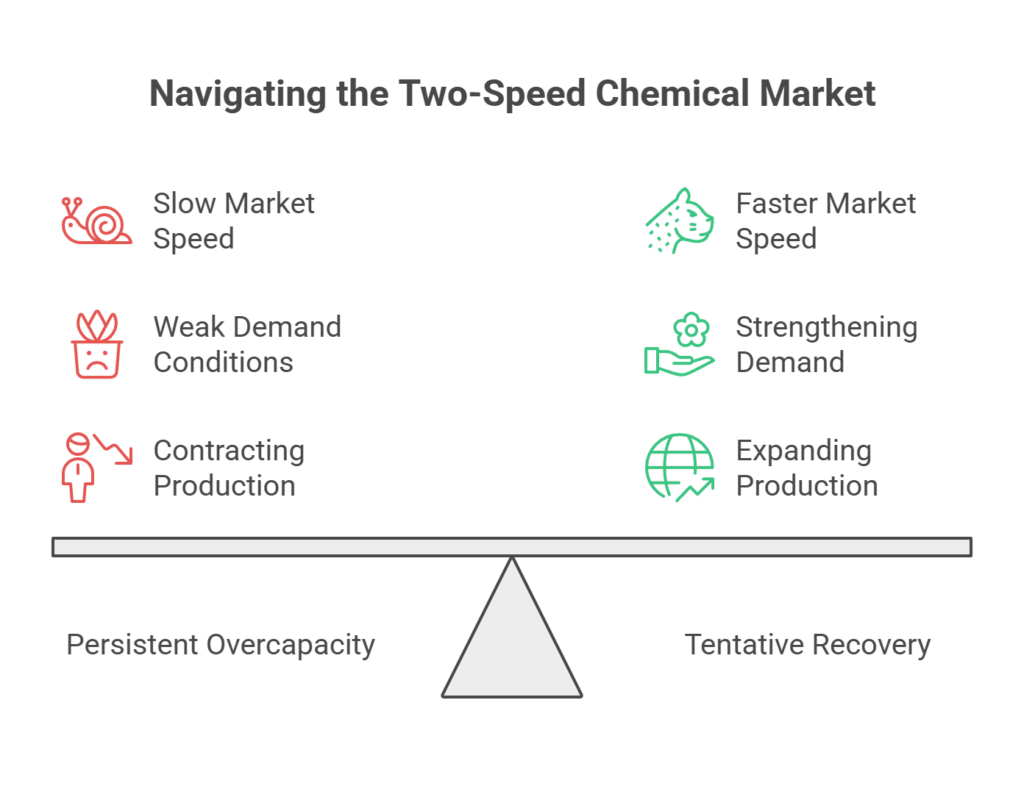

For procurement leaders trying to read the chemical market in 2026, the signals appear hopelessly contradictory. On one side, the industry is wrestling with structural overcapacity, compressed margins, and an ongoing wave of plant closures. On the other, demand indicators have begun to strengthen, suggesting a recovery is taking shape. Add a backdrop of tariff volatility and serious shipping disruption, and the result is a market moving at two speeds simultaneously.

Understanding this two-speed dynamic is essential, because it changes the calculus of how companies should source their chemicals. In a market this unpredictable, rigidity is the real risk, and surplus and off-spec inventory has emerged as one of the most effective hedges available.

Signal One: Persistent Overcapacity

The first speed of the market is slow, and it has been slow for a while. The chemical industry entered a prolonged downcycle, and forecasts for global chemical production growth remain weak at roughly 2% for 2026, with US production volumes expected to contract slightly [1].

The core problem is structural overcapacity in basic chemicals. New ethylene and polyethylene capacity continues to come online in low-cost regions, and self-sufficiency policies in China keep adding supply [1]. This persistent overcapacity pressures operating rates and squeezes margins, which is why major producers have continued aggressive cost-cutting, restructuring, and plant closures into 2026 [2]. By this measure, the market looks firmly like a downturn.

Signal Two: A Tentative Recovery

The second speed of the market is faster, and it is newer. According to S&P Global Market Intelligence, demand conditions in the chemicals sector improved in April 2026, with global demand for chemicals and chemical-related products showing signs of strengthening, driven by increased new orders and a faster pace of production growth [3].

Broader manufacturing data echoed this turn. US manufacturing activity reached multi-year highs in mid-2026, with new orders expanding for several consecutive months and chemical products cited among the growth contributors [4]. By this measure, the market looks like the early stage of a rebound.

Both readings are accurate. Some segments and regions are still contracting under the weight of oversupply, while others are seeing genuine demand recovery. The market is not uniformly up or down; it is two-speed.

The Volatility Layer: Tariffs and Shipping

What makes the two-speed market genuinely difficult to manage is the volatility layered on top of it.

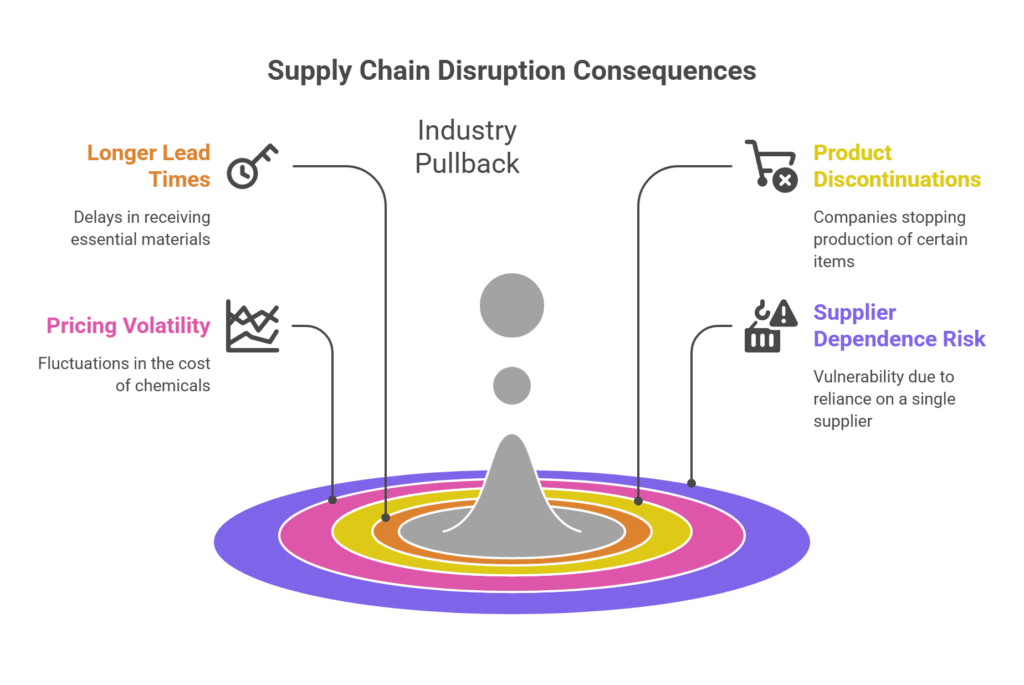

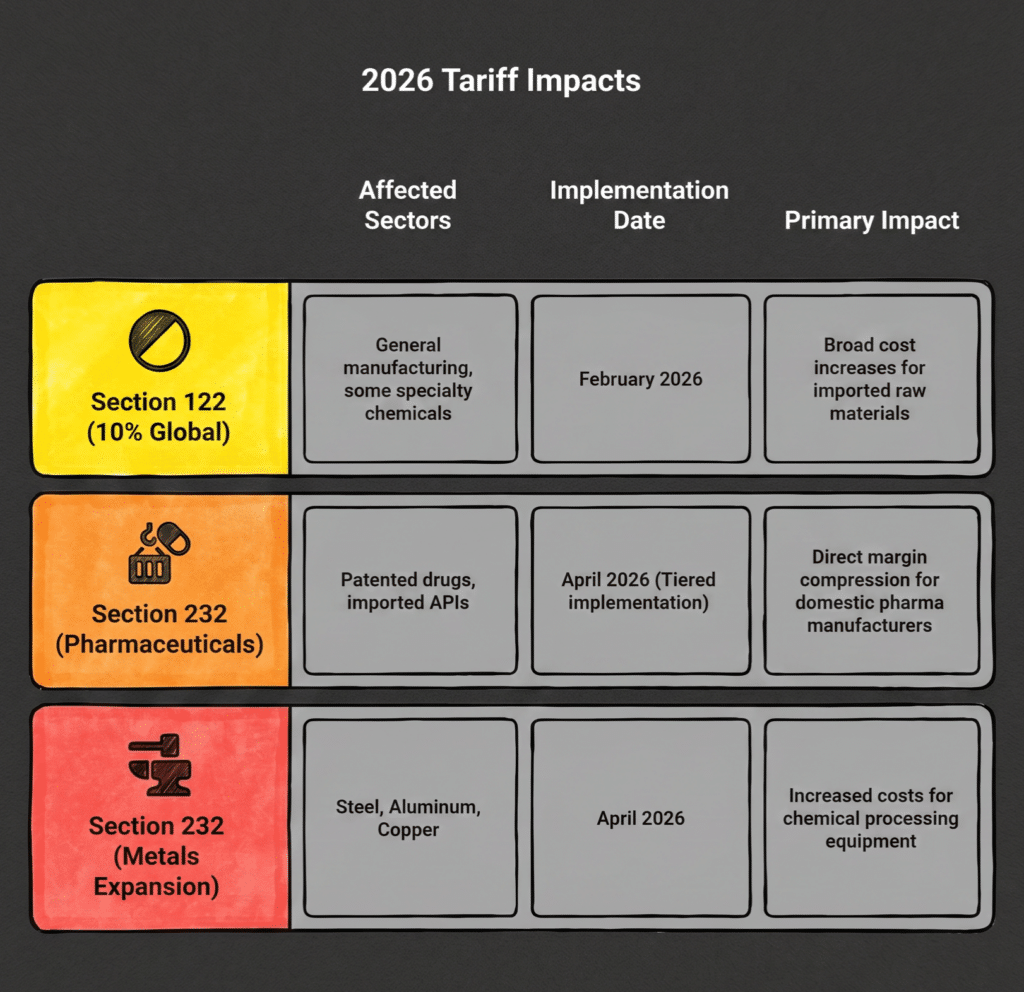

Trade policy has been highly reactive in 2026, with shifting tariffs reshaping sourcing decisions and adding cost uncertainty to imported materials [1]. At the same time, the physical supply chain has been disrupted. Tensions around the Strait of Hormuz and the Red Sea have pushed major carriers to reroute vessels, driving up freight costs and extending transit times on key global chemical trade lanes [5]. Reroutes around the Cape of Good Hope add one to three weeks of transit and significant conflict-related surcharges to affected shipments [6].

For a procurement team, this is the worst of both worlds: a market where you cannot confidently predict demand or price, and a supply chain where you cannot confidently predict delivery.

Why Rigidity Is the Real Risk

In a stable, predictable market, the optimal procurement strategy is often to lock in long-term contracts with primary suppliers and run lean inventory. That logic breaks down in a two-speed, volatile market.

If you over-commit to virgin supply contracts and demand softens in your segment, you are stuck with expensive material. If you run too lean and your segment recovers while freight lanes are disrupted, you cannot get supply when you need it. If your imported feedstock is hit by a sudden tariff or a rerouted vessel, your costs and timelines blow out overnight. Rigidity, in any direction, becomes a liability.

The defining capability in this environment is flexibility, the ability to pivot sourcing quickly as conditions shift. This is precisely what a surplus sourcing strategy provides.

Why Surplus Is the Smartest Hedge

Surplus and off-spec chemicals function as a hedge for three reasons that map directly onto the risks of the two-speed market.

First, surplus inventory is decoupled from international freight volatility. Domestic surplus material is already within the country, so it sidesteps the Hormuz and Red Sea reroutes, the surcharges, and the extended transit times affecting imported chemicals [5][6]. When ocean freight becomes unpredictable, ready domestic material becomes invaluable.

Second, surplus pricing is insulated from tariff swings. Because off-spec and surplus chemicals are priced on their surplus status rather than virgin commodity indices, they are largely shielded from sudden tariff-driven cost increases on imported virgin material. This gives buyers a degree of price predictability that imported feedstocks simply cannot offer in 2026.

Third, surplus is fast. The inventory is already manufactured and ready to ship, which directly counters the longer lead times created by ongoing plant closures across the industry [2]. When a segment recovers faster than expected, the ability to source ready material without waiting on new production is a decisive advantage.

This is the key reframe. In a predictable market, surplus chemicals are primarily a way to reduce cost. In a two-speed, volatile market like 2026, surplus is a way to stay supplied and stay flexible. It is risk management, not just a discount.

Building the Hedge Into Your Strategy

The producers will keep closing plants while demand signals keep flickering between contraction and recovery. The companies that thrive will be those that stop trying to predict which signal wins and instead build a procurement strategy resilient to both.

That means diversifying away from single-supplier, single-route dependence and developing relationships with surplus chemical partners who can provide real-time visibility into available domestic and international inventory. At Surplus International, we help manufacturers turn the uncertainty of the two-speed market into an advantage, matching ready surplus and off-spec inventory with the buyers who need a reliable, cost-stable, fast-moving source of supply. In 2026, that is not a fallback option. It is the smartest hedge on the board.

References

[1] Deloitte Insights. (2025). 2026 Chemical Industry Outlook. Deloitte. Retrieved from https://www.deloitte.com/us/en/insights/industry/chemicals-and-specialty-materials/chemical-industry-outlook.html

[2] Alliance Chemical. (2026). Chemical Industry Faces Another Year of Deep Cutbacks as Major Producers Slash Thousands of Jobs. Retrieved from https://alliancechemical.com/blogs/news/chemical-industry-faces-another-year-of-deep-cutbacks-as-major-producers-slash

[3] S&P Global Market Intelligence. (2026). Demand Conditions Improve in Chemicals Sector in April 2026. Retrieved from https://www.spglobal.com/en/research-insights/market-insights/energy-commodities/chemicals

[4] IndustrialSage. (2026). US Manufacturing PMI Hits a Four-Year High in May 2026. Retrieved from https://www.industrialsage.com/us-manufacturing-pmi-hits-a-four-year-high-in-may-2026/

[5] S&P Global Ratings. (2026). European Chemicals: Hormuz Reopening Could Offset Fading Middle East Tailwinds. Retrieved from https://www.spglobal.com/ratings/en/regulatory/article/european-chemicals-hormuz-reopening-could-offset-fading-middle-east-tailwinds-s101687428

[6] Air 7 Seas. (2026). How the 2026 War Impacts Global Trade: Shipping Disruptions and Fixes for US Importers. Retrieved from https://air7seas.com/blog/how-the-2026-war-impacts-global-trade-shipping-disruptions-fixes-for-us-importers