Insights on the Surplus & Off-Spec Chemical Market

Welcome to the SUR+ International knowledge hub, where we explore the forces shaping the global chemical industry and the growing role of surplus redistribution. From shifting tariff landscapes and plant closures to safe storage, sustainability, and supply chain resilience, our articles unpack the trends, risks, and opportunities that matter most to manufacturers, procurement leaders, and sustainability teams.

Whether you’re holding excess inventory you didn’t know was a recoverable asset, or sourcing reliable off-spec materials as a hedge against volatility, these articles offer practical perspective grounded in real market data. Dive in to discover how turning surplus chemicals into value can strengthen your bottom line, reduce your energy footprint, and build a more resilient operation.

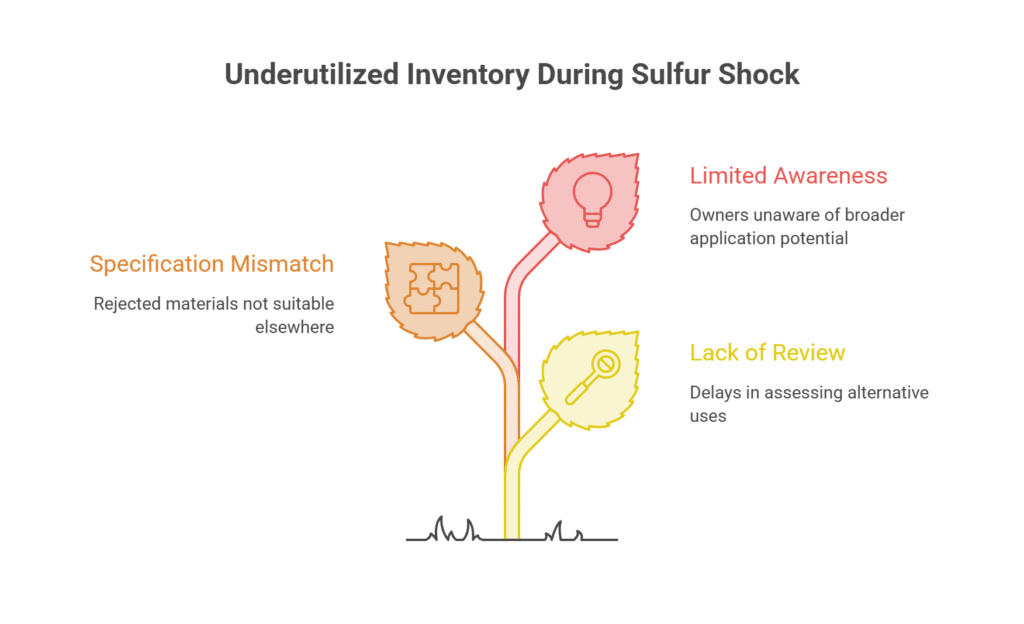

In our previous analysis of the 2026 sulfur disruption, we considered how a supply shock can change the strategic value of dormant chemical inventory. A well-characterized secondary batch may provide another sourcing option when a primary route becomes constrained- but only if the industry can find, assess, document, and transport that material responsibly.

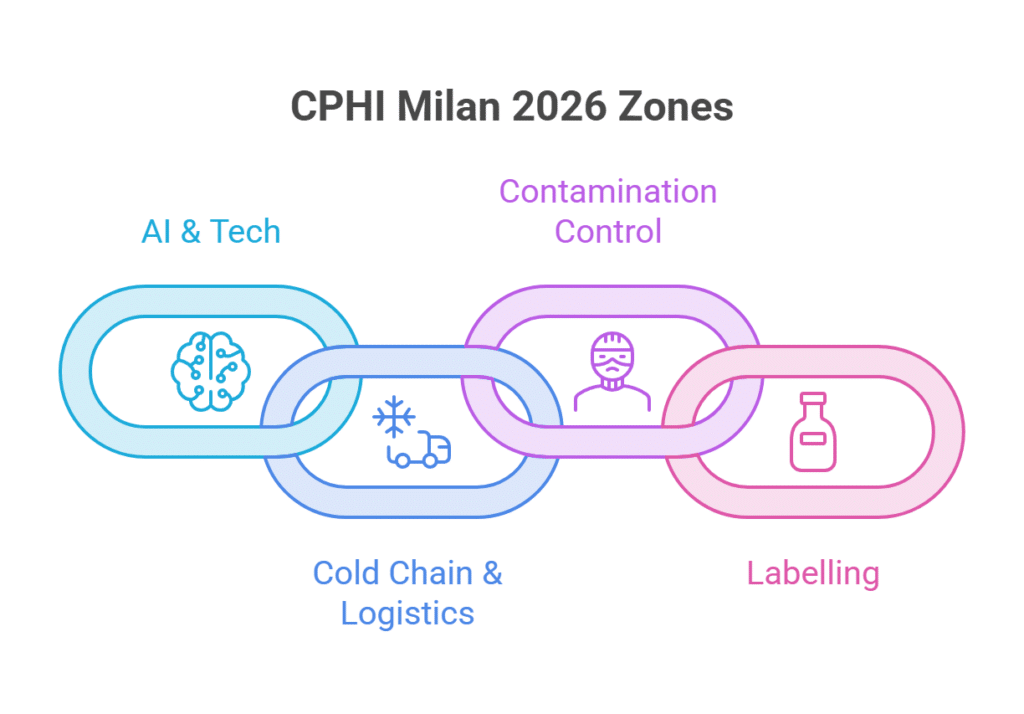

That is why the agenda for CPHI Milan 2026 is especially relevant. The event will take place at Fiera Milano from 6-8 October 2026 and includes new zones for AI & Tech, Cold Chain & Logistics, Contamination Control, and Labelling.1

The global chemical industry is accustomed to price cycles, but the supply disruptions of 2026 have exposed a more fundamental vulnerability: many value chains still depend on a small number of production regions and transport corridors for essential feedstocks.

Sulfur is a clear example. The Middle East accounts for approximately one-quarter of global sulfur supply, while about half of global seaborne sulfur trade passes through the Strait of Hormuz.1 The region’s importance extends far beyond sulfur itself. Sulfur is a key feedstock for sulfuric acid, which is essential to phosphate-fertilizer production and the processing of copper, lithium, cobalt, nickel, rare earths, and other critical minerals.1

The global chemical industry is currently managing one of the most complex regulatory transitions in its history: the phase-out and restriction of per- and polyfluoroalkyl substances (PFAS), commonly known as “forever chemicals.”

By mid-2026, the regulatory pressure has reached a critical inflection point. In June 2026, the European Chemicals Agency (ECHA) published the results of its draft consultation regarding the comprehensive PFAS restriction proposal, revealing deep industry concern-particularly from the electronics and semiconductor sectors, which accounted for the largest share of the 3,511 submitted comments [1]. Concurrently, the European Union’s Packaging and Packaging Waste Regulation (PPWR) is set to enforce strict PFAS limits on food-contact packaging starting August 12, 2026 [2].

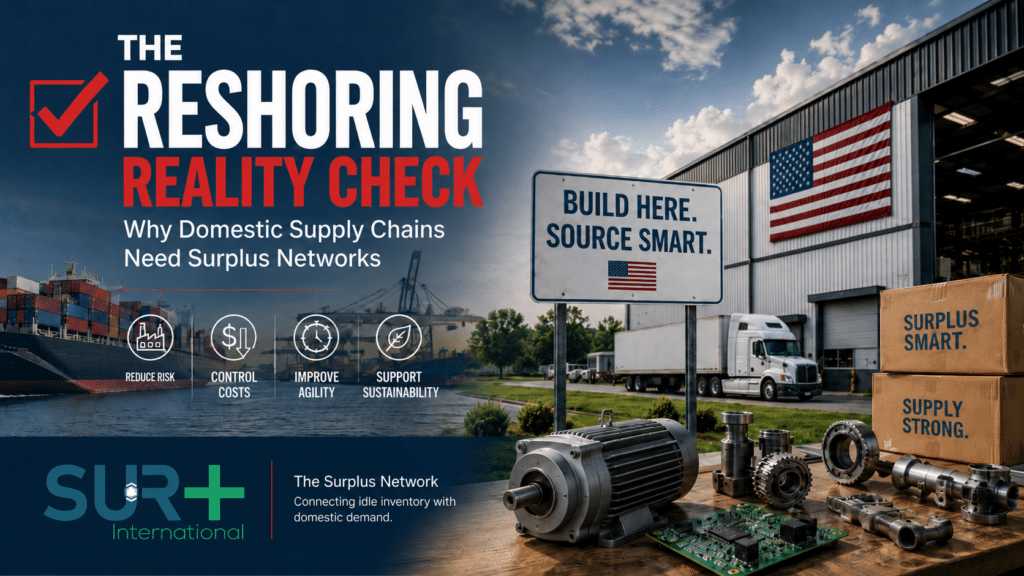

The manufacturing landscape in 2026 is undergoing a profound geographic shift. Driven by geopolitical tensions, shifting trade policies, and the painful lessons of recent global disruptions, companies are bringing production closer to home. Recent data indicates that 244,000 reshoring jobs have been created, and 56% of large companies across Europe and the USA have invested in reshoring or nearshoring production in the past year [1].

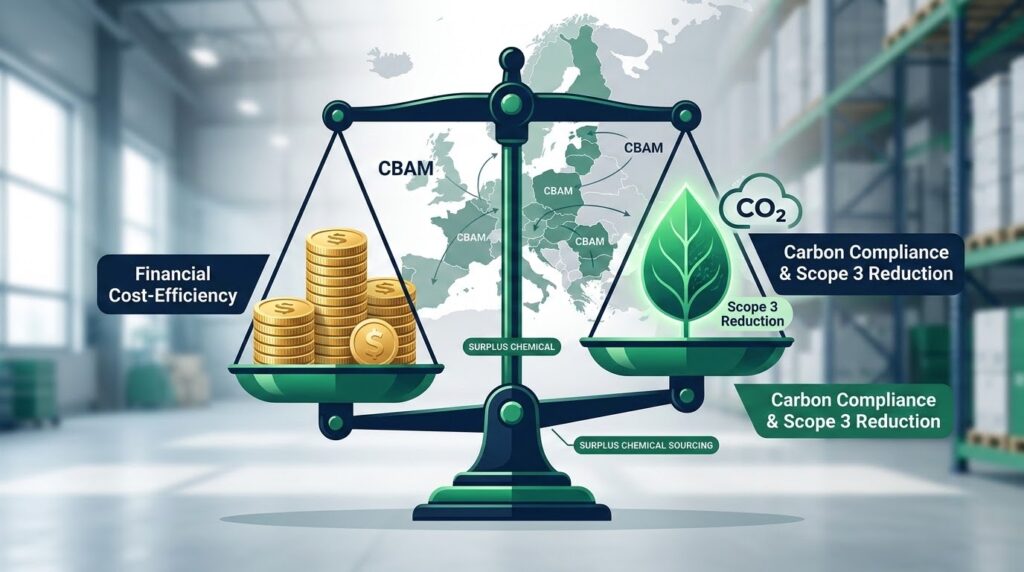

For most of its history, the case for buying surplus and off-spec chemicals has been a financial one. Surplus material is cheaper than virgin product, it eliminates disposal costs, and it frees up warehouse space. These are real and durable advantages. But in 2026, a new and arguably more powerful argument has emerged, one that has little to do with the price tag and everything to do with regulation.

The 2026 chemical market is defined by contradictory signals, creating a “two-speed” landscape for procurement teams.

Structural overcapacity suppresses some segments, while manufacturing growth drives a tentative recovery in others. Layered on this complexity are unpredictable tariffs and severe shipping disruptions that make rigid supply chains a significant liability. In this environment, relying solely on long-term virgin contracts exposes your organization to unnecessary risk.

Instead, smart procurement leaders are pivoting toward flexibility to maintain reliable supply lines. Surplus and off-spec inventory has emerged as a critical hedge, offering stability where standard chains cannot.

Discover why it is time to rethink your sourcing strategy to stay competitive and supplied throughout the year!

The chemical industry in 2026 is defined by a great sorting. Faced with persistent overcapacity in basic chemicals, compressed margins, and a sluggish demand recovery, the world’s largest producers are making a decisive strategic move: they are walking away from low-margin commodity production and reorienting their portfolios toward higher-value specialty chemicals.

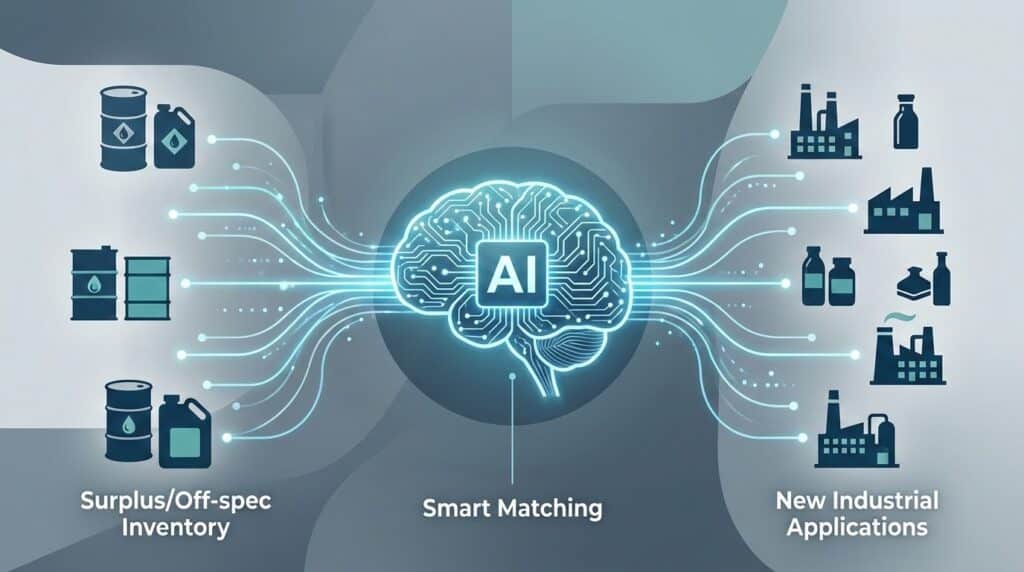

The global chemical industry is in the midst of a profound restructuring. Driven by margin pressures, shifting tariffs, and a drive toward portfolio optimization, major producers are closing plants and exiting commodity lines. This consolidation is generating unprecedented volumes of high-quality surplus and off-specification chemicals. Yet, despite the sheer volume of available material and the urgent need for cost-effective feedstocks among global buyers, the surplus chemical market has remained surprisingly analog.

In an era where global supply chains are increasingly scrutinized for their environmental footprint and resilience, understanding fundamental green chemistry principles has become a strategic imperative, particularly within the healthcare and pharmaceutical sectors. For procurement officers like Jordi and Alessio, navigating volatile markets while balancing cost, quality, and compliance is a constant challenge. For sustainability leaders like Alessia, the mandate to reduce CO₂e emissions and embed sustainable practices across complex value chains demands innovative solutions. Green chemistry offers a powerful framework to address these very concerns, moving beyond mere compliance to proactive innovation that delivers both environmental and economic benefits.