How the Strait of Hormuz Closure Redefines Chemical Surplus Markets

The de facto closure of the Strait of Hormuz, following military action in the Persian Gulf in late February 2026, has sent a shockwave across global energy and chemical markets. For buyers and sellers in the chemical surplus industry, this disruption is not just a headline- it is a fundamental test of supply chain resilience and a critical inflection point that creates both unprecedented challenges and significant opportunities.

As a strategic chokepoint for global trade, the Strait of Hormuz facilitates the daily passage of approximately 20% of the world’s crude oil and a significant volume of petrochemicals, including around one-third of global urea and 44% of sulfur exports [1]. With maritime traffic now at a standstill, insurance providers withdrawing coverage, and shipping giants rerouting fleets around the Cape of Good Hope, the ripple effects are being felt across every link in the chemical value chain [2].

This analysis explores the immediate and structural impacts of the Hormuz closure on key energy-related chemicals and examines how these disruptions are reshaping the landscape for the chemical surplus market. For procurement leaders and supply chain managers, understanding this new reality is essential for navigating risk and unlocking strategic value.

The Immediate Fallout: Production Shutdowns and Price Volatility

The most immediate consequence of the escalating conflict has been the shutdown of major production facilities. On March 3, 2026, QatarEnergy, the world’s largest liquefied natural gas (LNG) exporter, announced a halt to all LNG production following drone strikes on its facilities. Crucially, this shutdown extended to its downstream operations, ceasing the production of urea, polymers, and methanol [3].

This single event has removed a massive volume of key chemicals from the global market, compounding the logistical nightmare of the strait’s closure. The impact on pricing has been swift and severe:

- Oil Prices: Brent crude futures surged by 10-13% in the immediate aftermath, creating a powerful headwind for the entire petrochemical industry, where crude oil derivatives like naphtha are primary feedstocks [4].

- Freight Costs: With the world’s largest shipping lines suspending passage through the region, freight and insurance costs have skyrocketed. War-risk premiums have surged, and some carriers have imposed security surcharges of $3,000-$4,000 per container, a cost that is inevitably passed down the supply chain [5].

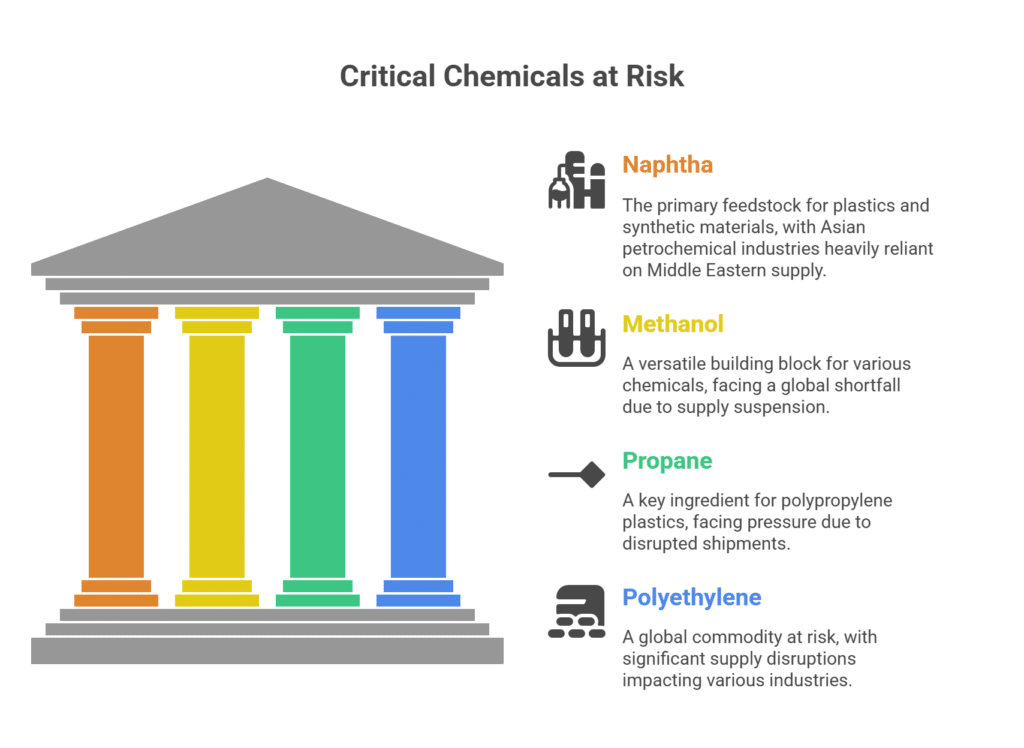

- Naphtha: As a key feedstock for plastics and other organic chemicals, naphtha prices in Asia jumped by nearly 11% in early March, with traders estimating that up to 2 million metric tons of March-loading cargoes from the Middle East could be affected [6].

This extreme volatility has forced many market participants into a holding pattern, withdrawing offers and pausing trades as they struggle to price in the unprecedented risk. It is in this environment of uncertainty and scarcity that the strategic importance of the chemical surplus market comes into sharp focus.

Impact on Key Energy-Related Chemical Value Chains

The disruption is not uniform; specific chemical value chains are experiencing acute and distinct pressures. For surplus chemical traders, understanding these nuances is key to identifying opportunities.

Methanol and Solvents: A Looming Global Deficit

The Middle East is a powerhouse in methanol production. Iran is the world’s second-largest producer, exporting over 80% of its 9-10 million metric ton annual output, primarily to Asia. The shutdown of QatarEnergy’s methanol plants further constricts supply. This dual disruption threatens to create a structural global deficit of several million tons, sending prices for methanol and its derivatives- such as formaldehyde and acetic acid- soaring [7].

For companies holding surplus inventories of methanol or other solvents (like European hydrocarbon solvents, which have already seen spot offers jump by 10%), this scarcity transforms a once-dormant asset into a highly valuable commodity. Buyers in Asia, cut off from their primary suppliers, will increasingly look to alternative sources, including surplus markets in Europe and North America.

Polymers: A Market on Pause

The polymer market in the Middle East, a region that accounts for roughly 20% of global polypropylene (PP) exports, has effectively been frozen. Major producers have withdrawn all offers, and force majeure has been declared on polypropylene supplies from key Saudi facilities [5]. With no shipments leaving the region, buyers in Turkey, Africa, and India who rely on these supplies are facing imminent shortages.

This creates a significant opening for sellers with surplus polyethylene (PE) and polypropylene (PP) inventory. As primary production stalls, the value of existing, readily available surplus material skyrockets. Procurement managers who once saw surplus as a secondary option will now view it as a critical lifeline to maintain production continuity.

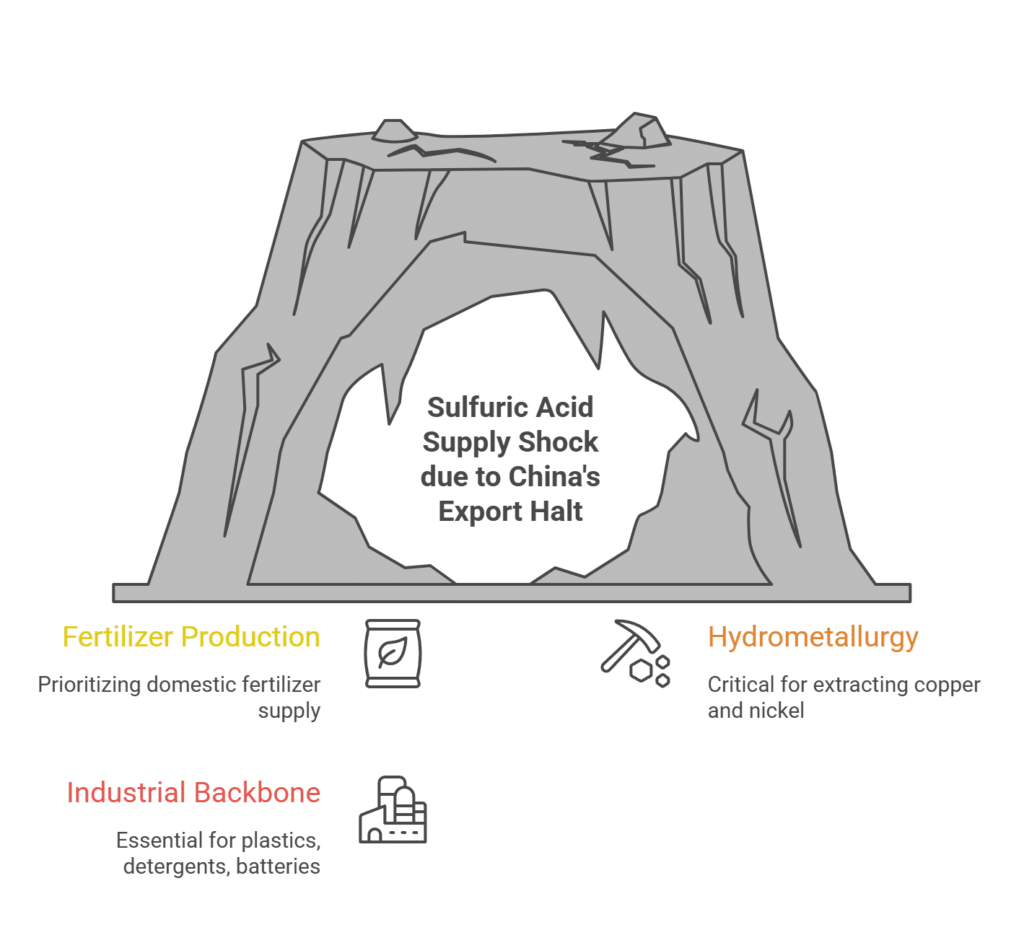

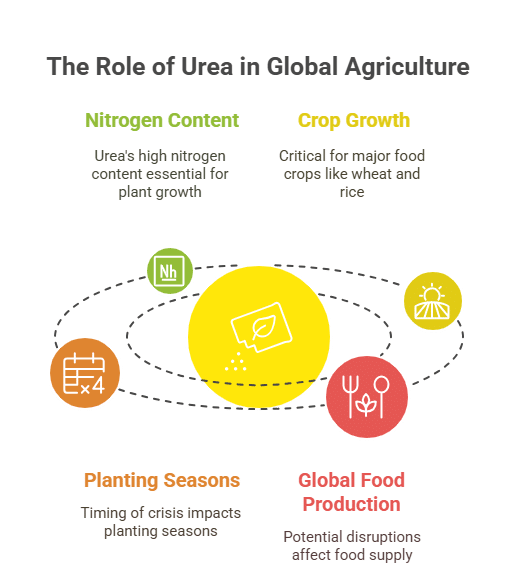

Fertilizers: A Direct Threat to Food Security

The Strait of Hormuz is a vital artery for the global fertilizer trade. With approximately 33% of global urea and 44% of sulfur exports now trapped, the impact on global agriculture could be severe [1]. QatarEnergy’s decision to halt urea production further exacerbates the shortage. Prices for urea have already surged in key markets like the U.S. (NOLA) ahead of the critical spring planting season [8].

This disruption highlights the strategic value of surplus fertilizer components. For agricultural businesses and blenders, securing access to surplus ammonia, urea, or sulfur could be the key to navigating the coming months of supply uncertainty and price hikes.

The Strategic Opportunity for Surplus Chemical Buyers and Sellers

In a stable market, surplus chemicals are often viewed as a way to optimize costs or manage waste. In a crisis of this magnitude, their role is transformed. Surplus inventory becomes a source of supply chain resilience. As one procurement executive has noted, “In procurement, it’s not just about cost; it’s about building resilient, compliant, and innovative supply chains that secure our future.” The Hormuz crisis has made this sentiment an immediate operational reality.

For Sellers: Companies in North America and Europe holding surplus inventory now possess a strategic asset. What was once a line item for storage costs or potential disposal can now be monetized at a premium. That off-spec batch, discontinued product line, or excess stock from a canceled order is no longer a liability- it is a solution to a global supply chain problem. The significant global price increases of recent days mean your surplus material is worth substantially more than it was just weeks ago. Engaging with a specialist like Sur+ International enables you to accurately price and market this inventory to a global network of motivated buyers who are actively seeking alternatives to disrupted primary supply.

For Buyers: For procurement managers in Asia, Africa, and other import-dependent regions, the traditional supply chain has been broken. The focus must shift from long-term contracts to immediate availability. Unlike primary production, which is stalled indefinitely, surplus inventory is on the ground and ready to ship- a critical advantage when every day of downtime carries a financial cost. Furthermore, the crisis has exposed the systemic danger of concentrating sourcing within a single geographic region. Diversifying procurement through the surplus market in Europe and North America provides immediate resilience and reduces exposure to Middle East volatility.

The New Landscape: A Playbook for a Disrupted Market

This new environment requires a new strategy. Both buyers and sellers must adapt to the realities of a supply-constrained world.

| Stakeholder | Actionable Strategy |

|---|---|

| Sellers with Surplus | 1. Conduct a comprehensive audit of all non-performing chemical inventory. Identify everything from off-spec materials to expired R&D samples. |

| 2. Partner with a global surplus specialist. Leverage their network and expertise to connect with buyers in high-demand regions like India and the Far East. | |

| 3. Emphasize availability and speed. In this market, the ability to ship immediately is a powerful competitive advantage. | |

| Buyers Facing Shortages | 1. Proactively engage with the surplus market. Do not wait for production lines to stop. Secure alternative supplies now to mitigate future disruptions. |

| 2. Be flexible on specifications. Off-spec or near-prime surplus materials can often be a perfectly viable substitute, especially when primary materials are unavailable at any price. | |

| 3. Build relationships with surplus suppliers. Establish connections now to ensure you are a preferred customer for future opportunities. |

Beyond the Crisis: The Enduring Value of a Circular Supply Chain

The Strait of Hormuz crisis is an acute shock, but it underscores a chronic vulnerability in the global chemical supply chain. The linear model of “produce, use, dispose” is inherently fragile. This event serves as a powerful catalyst for embracing a more resilient, sustainable, and circular model, where surplus and off-spec materials are not treated as waste, but as a continuous and valuable resource stream.

By turning today’s surplus into tomorrow’s supply, companies can not only navigate the immediate crisis but also build a more robust and profitable supply chain for the future. The shockwave from the Strait of Hormuz will eventually subside, but the strategic lessons it imparts- about the value of resilience, the importance of diversification, and the power of the circular economy- will resonate for years to come.

References

[1] U.S. Energy Information Administration (EIA). “Strait of Hormuz: Critical Oil Chokepoint.” Today in Energy, 16 June 2025.

[2] Reuters. “Global oil and gas shipping costs surge as Iran vows to close Strait of Hormuz.” 2 March 2026.

[3] QatarEnergy. “QATARENERGY TO STOP DOWNSTREAM PRODUCTION.” News Release, 3 March 2026.

[4] ResourceWise. “Shipping Disruption in the Persian Gulf Sends Oil Higher, Raising Immediate Feedstock Risk for Global Petrochemical Markets.” 2 March 2026.

[5] S&P Global. “FACTBOX: Chemical market navigates disruptions as US-Iran conflict triggers upstream production outages.” 2 March 2026.

[6] OPIS. “Asia Benzene Jumps Nearly 8% as Iran Crisis Roils Feedstock, Freight Markets.” 3 March 2026.

[7] Blooming Global. “Middle East Conflict Disrupts Global Chemical Trade.” 4 March 2026.

[8] Argus Media. “Nola urea prices surge on US-Iran conflict.” 2 March 2026.