The Tariff-Driven Inventory Crisis: Why Reshoring Requires a Strategic Surplus Solution

The global chemical industry is navigating a period of profound transformation. Driven by geopolitical tensions, shifting trade policies, and the pursuit of supply chain resilience, companies across North America are fundamentally rethinking how and where they source their materials. However, this transition is not without its growing pains. One of the most significant, yet often overlooked, challenges facing chemical manufacturers today is the tariff-driven inventory crisis, a phenomenon that has left companies burdened with excess stock, blocked capital, and a strategic dilemma that demands a new kind of solution.

The Front-Loading Hangover

The roots of this crisis can be traced back to the volatile trade environment of early 2025. Faced with the looming threat of increased tariffs under the new US trade policy regime, many procurement teams adopted a defensive strategy: front-loading. In March 2025 alone, US chemical imports surged to over $20 billion, the highest level in more than three years [1]. Buyers rushed to secure materials before costs escalated, prioritizing immediate availability over long-term demand forecasting.

While this strategy provided short-term security, it created a significant long-term problem. As demand softened later in the year and the anticipated supply shocks partially stabilized, companies found themselves sitting on massive stockpiles of raw materials. By April 2025, imports had dropped sharply, leaving teams with bloated inventories and facing weaker demand [1]. This stop-start pattern of procurement repeated throughout the year, reshaping freight seasonality and making budgeting, as one industry analyst put it, “little more than informed guesswork.”

The consequences are now compounding. The US Trade Representative initiated new Section 301 investigations in March 2026 targeting structural excess manufacturing capacity in several countries [2], signaling that tariff uncertainty is far from over. For procurement leaders, this means the conditions that created the inventory crisis are not temporary; they are structural.

The Reshoring Reality Check

Simultaneously, the industry is witnessing a fundamental structural shift toward reshoring and nearshoring. To mitigate the risks associated with long, complex global supply chains, manufacturers are increasingly localizing their operations. US chemical manufacturing establishments grew by 10.2% between 2017 and 2022, from 13,571 to 14,961, even as the broader manufacturing sector contracted [3]. Chemical construction spending surged to $45.6 billion in early 2026, an 11.5% year-over-year increase [4], underscoring the industry’s commitment to building domestic capacity.

While reshoring offers undeniable benefits in terms of resilience and control, it also necessitates a rationalization of existing inventory. As production models become more streamlined and localized, the materials stockpiled during the front-loading phase may no longer align with current manufacturing needs. Formulations change, product lines are discontinued, and the sheer volume of stored chemicals becomes a logistical and financial burden. The result is a growing volume of slow-moving, out-of-date, or off-specification stock that sits idle in warehouses across the continent.

The True Cost of Inaction

For chemical manufacturers, holding onto surplus inventory is not a neutral position; it is an active drain on resources. The following table illustrates the multifaceted costs associated with excess chemical stock:

| Cost Category | Description | Impact |

|---|---|---|

| Blocked Working Capital | Capital tied up in unused inventory cannot be deployed for innovation, expansion, or operational improvements. | Reduced financial agility and missed growth opportunities |

| Storage and Maintenance | Warehousing chemicals, particularly hazardous materials, requires specialized facilities, insurance, and ongoing compliance monitoring. | Significant and recurring overhead costs |

| Degradation and Expiry | Chemicals have a finite shelf life. As materials age, their quality degrades, eventually rendering them unusable. | Asset value erosion leading to total write-offs |

| Disposal Costs | Traditional disposal of expired or off-spec chemicals involves hazardous waste handling, regulatory compliance, and environmental fees. | High one-time costs with zero return on investment |

| Environmental Liability | Improper disposal or prolonged storage of chemicals can create regulatory risk and reputational damage. | Potential fines and ESG reporting complications |

The cumulative effect of these costs is substantial. For many companies, the surplus sitting in their warehouses represents millions of dollars in locked-up value that is actively depreciating. In an industry already contending with a prolonged downturn, where major players like BASF posted a 38.8% decline in earnings in 2025 [5], the ability to recover capital from idle assets is not just advantageous; it is essential.

From Liability to Strategic Asset

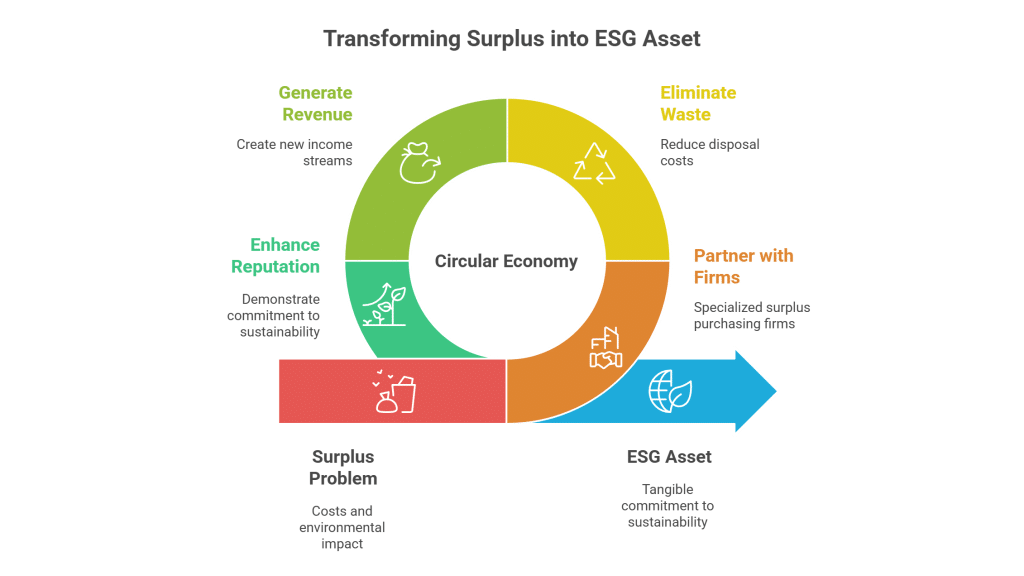

The traditional approach to surplus chemicals, costly waste disposal, is no longer viable, neither financially nor environmentally. In an era where the circular economy is moving from aspiration to regulation, and where ESG performance is increasingly linked to financial valuation, companies must adopt a more strategic approach to inventory management.

This is where strategic surplus management provides a critical solution. Rather than viewing excess inventory as a problem to be disposed of, forward-thinking companies are recognizing it as an asset to be monetized. The global market for surplus chemicals is substantial and growing, driven by demand from manufacturers in developing economies who are actively seeking high-quality, cost-effective raw materials.

At SUR+ International, we specialize in this exact transformation. Our global network connects North American and European manufacturers burdened with excess stock to buyers in high-growth markets, particularly in India and the Far East, where demand for these materials remains robust. By partnering with a dedicated surplus management partner, companies can achieve three critical outcomes simultaneously:

First, capital recovery. A streamlined process for assessing, valuing, and purchasing surplus inventory injects much-needed liquidity back into the business. Instead of writing off inventory, companies receive payment for materials that still hold significant value in other markets.

Second, cost elimination. By removing surplus stock from your facilities, you eliminate the ongoing costs of storage, insurance, and maintenance. You also avoid the exorbitant fees associated with hazardous waste disposal, which can run into hundreds of thousands of dollars for large volumes.

Third, sustainability advancement. Repurposing surplus chemicals is a core tenet of the circular economy. By giving these materials a second life in a different industry or geography, companies prevent valuable resources from entering the waste stream. This directly supports ESG goals, improves sustainability reporting metrics, and reinforces green corporate policies.

A New Playbook for a New Era

The tariff-driven inventory crisis is a complex challenge, but it also presents a unique opportunity for strategic optimization. As the chemical industry continues to evolve under the pressures of trade volatility, reshoring, and sustainability mandates, the ability to efficiently manage and monetize surplus inventory will become a key differentiator between companies that merely survive and those that thrive.

The companies that will lead in this new era are those that recognize surplus chemicals not as waste, but as working capital waiting to be unlocked. They are the ones that integrate surplus management into their broader supply chain strategy, treating it as a proactive function rather than a reactive afterthought.

At SUR+ International, we are committed to helping companies navigate this transition. With over 10,000 customers worldwide and a track record of preventing 80% of materials from being destroyed or going unused, we have the global reach, the industry expertise, and the logistical capability to turn your overstock into opportunity.

If your organization is grappling with the consequences of tariff-driven inventory buildup, we invite you to explore how a strategic surplus partnership can transform your balance sheet and your sustainability profile. The first step is a conversation.

References

[1] Xeneta. (2026, March 23). The Price of Uncertainty: How Trade Volatility Is Breaking Chemical Supply Chains. https://www.xeneta.com/blog/the-price-of-uncertainty-how-trade-volatility-is-breaking-chemical-supply-chains

[2] Benesch Law. (2026, March 20). New 301 Tariffs Coming: Immediate Action Items For Supply Chains. https://www.beneschlaw.com/insight/new-301-tariffs-coming-immediate-action-items-for-supply-chains/

[3] U.S. Census Bureau. (2026, March 5). U.S. Chemical Manufacturers Grew Despite Overall Manufacturing Decline. https://www.census.gov/library/stories/2026/03/chemical-manufacturing.html

[4] Plastics Today. (2026, March 28). Chemical Industry Construction Spending Hits $45.6B. https://www.plasticstoday.com/materials/chemical-construction-spending-surges-amid-mixed-economic-signals

[5] American Chemical Society (C&EN). (2026, March 22). The Chemical Industry Promises Another Year of Cutbacks. https://pubs.acs.org/doi/10.1021/cen-10404-buscon2