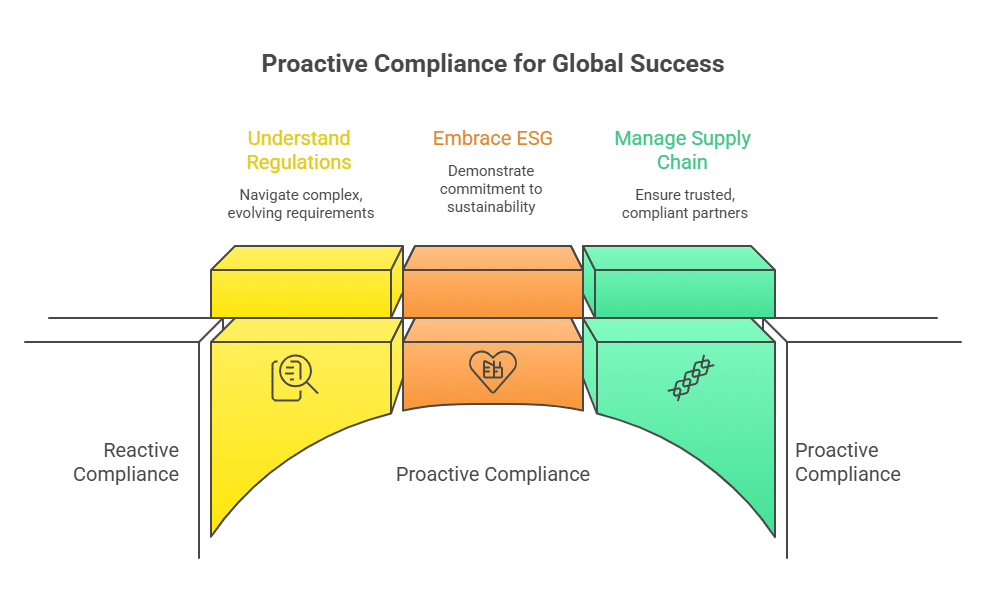

In the global chemical industry, regulatory compliance is often viewed as a defensive necessity- a complex and costly burden to be managed. But in 2026, with supply chains under constant pressure and market dynamics shifting at an unprecedented pace, this view is not just outdated; it’s a strategic liability. The smartest companies are discovering that proactive compliance is no longer just about avoiding fines. It’s about building a resilient, agile, and profitable business.

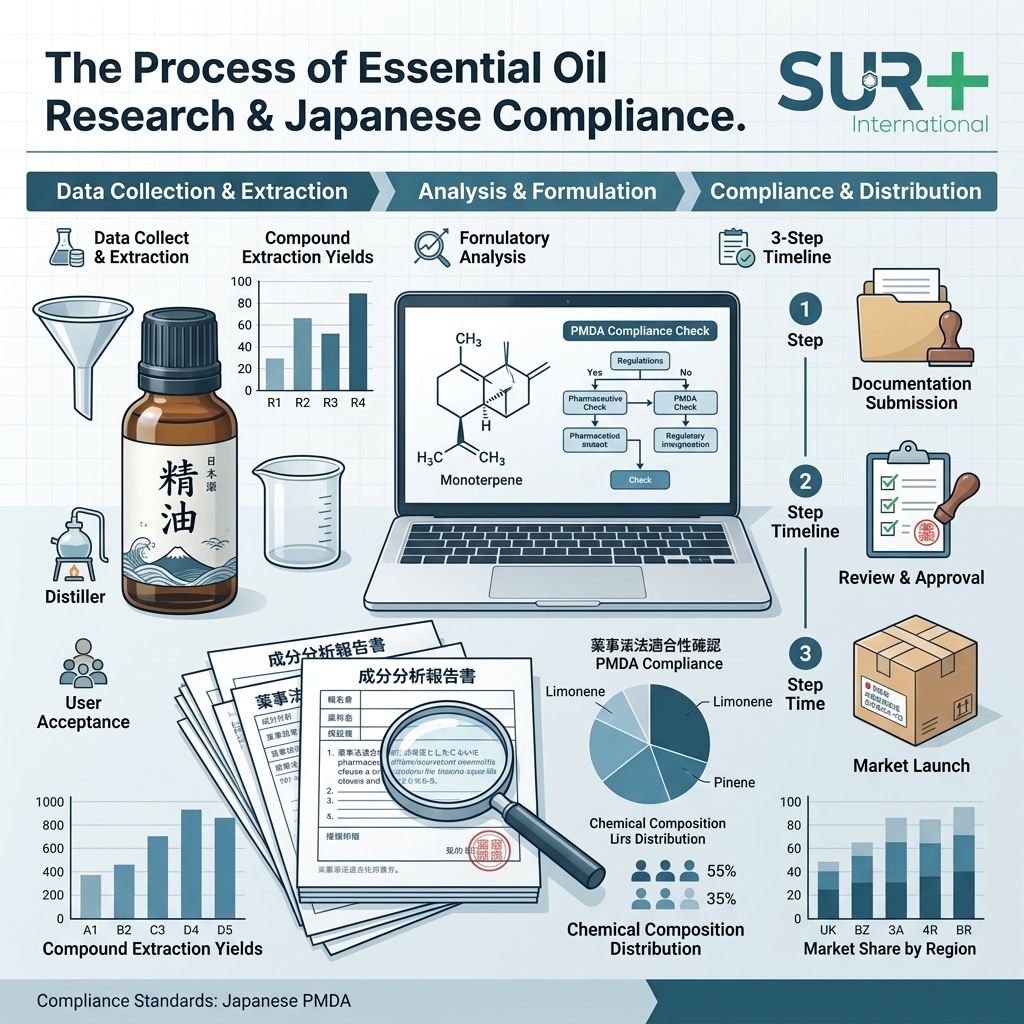

Comprehensive compositional analysis is therefore paramount to determine the regulatory status of an essential oil or its components. Misclassification or a lack of understanding can lead to significant delays, rejections, or even severe penalties. For exporters, this means not just understanding the oil’s botanical origin, but also its exact chemical fingerprint. It’s crucial for exporters to work closely with their Japanese importers, as the importer often holds primary responsibility for navigating CSCL notifications and registrations. The importer will rely heavily on accurate data from the exporter, including CAS numbers for all significant components, purity levels, and any known hazardous properties. Even minor impurities or additives within an essential oil blend can trigger unexpected regulatory hurdles if not properly identified and assessed under CSCL.

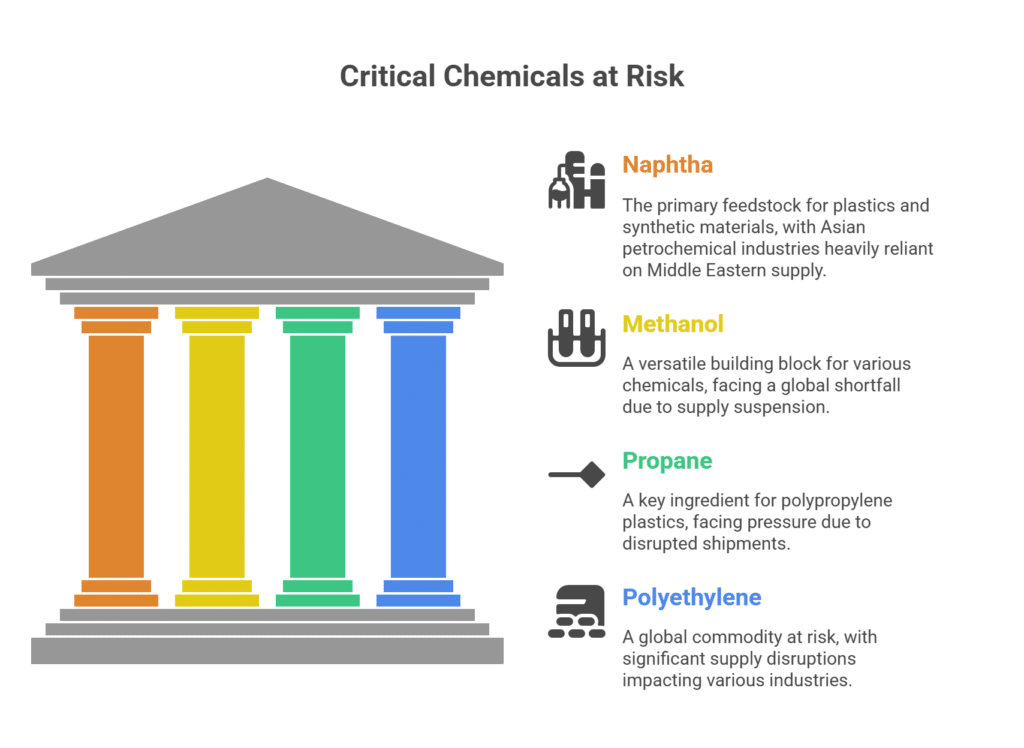

The global chemical supply chain is in a state of emergency. On February 28, 2026, the effective closure of the Strait of Hormuz, a vital artery for global trade, sent shockwaves through the industry. With approximately 30% of the world’s maritime oil trade and a significant portion of its petrochemical feedstock supply now choked off, procurement professionals are scrambling to navigate an unprecedented crisis [1].

For those who are prepared, this disruption presents not just a challenge, but a unique opportunity to rethink sourcing strategies and unlock the hidden value in the surplus chemical market.

This article provides a real-time guide to the specific chemicals most at risk and the actionable surplus alternatives that can be sourced today to maintain production and gain a competitive edge.

In the C-suite and among procurement leaders, strategic initiatives live and die by their financial merits. While the concepts of circular economy and sustainability are compelling, any new program must ultimately answer a fundamental question: What is the return on investment (ROI)? For surplus chemical derivatives, the answer is not just positive; it is transformative. Moving from a disposal cost model to a revenue generation model fundamentally alters the financial DNA of waste management, turning a long-standing cost center into a surprising new profit center.

In the high-stakes world of pharmaceutical and chemical manufacturing, the term “waste” has long been synonymous with cost. Disposal fees, regulatory burdens, and inventory write-offs have traditionally been accepted as the unavoidable price of doing business. But what if this paradigm is fundamentally flawed? What if the millions of dollars spent managing surplus and off-spec chemicals could be transformed into a significant revenue stream? This isn’t a futuristic fantasy; it’s a rapidly emerging reality driven by the “waste-to-wealth” movement, a cornerstone of the modern circular economy.

The shift from viewing surplus chemicals as “waste” to seeing them as “wealth” is a powerful strategic change. But for the operations managers, plant supervisors, and sustainability leaders on the ground, the question is more direct: How do we actually do it? The idea of launching a new chemical upcycling or derivatives program can seem daunting, fraught with operational hurdles and logistical complexities. However, with a structured approach and the right partnerships, it is an achievable and highly rewarding process improvement initiative.

The de facto closure of the Strait of Hormuz, following military action in the Persian Gulf in late February 2026, has sent a shockwave across global energy and chemical markets. For buyers and sellers in the chemical surplus industry, this disruption is not just a headline- it is a fundamental test of supply chain resilience and a critical inflection point that creates both unprecedented challenges and significant opportunities.